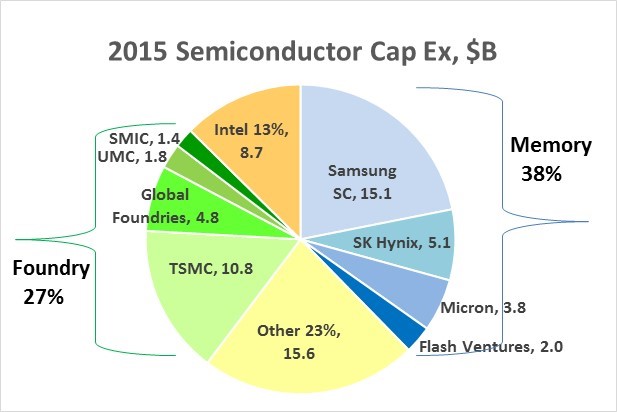

Semiconductor industry capital expenditures (capex) in 2015 are expected to be $69 billion in 2015, up 6% from $65 billion in 2014 according to IC Insights. We at Semiconductor Intelligence have compiled 2015 capex outlook by company. The major memory companies account for 38% of 2015 capex and the major foundries account for 27%.

Memory and foundry companies combined account for almost two-thirds of 2015 capex. The three largest spenders (Samsung, TSMC and Intel) add up to half of total capex. The table below shows capex for 2014 and projections for 2015. The projections are from the companies, Digitimes, and Semiconductor Intelligence (SC IQ). Digitimes forecast Samsung Semiconductor will spend $15.1 billion in 2015, up 13% from 2014. The midpoint of TSMC’s April guidance for 2015 is $10.8 billion, up 13%. This is down from TSMC’s January guidance of $11.5 billion to $12.0 billion, up 23% at the midpoint. Intel also reduced its guidance for 2015 capex from $11 billion in January (up 9%) to $8.7 billion in April (down 14%).

Semiconductor Capital Spending, US$ Billion |

|||||||

Company |

2014 |

2015 |

Change |

Notes on 2015 forecast |

|||

Samsung SC |

13.3 |

15.1 |

13% |

Digitimes, April 2015 |

|||

TSMC |

9.5 |

10.8 |

13% |

down from $11.8 B in Jan. 2015 |

|||

Intel |

10.1 |

8.7 |

-14% |

down from $11B in Jan. 2015 |

|||

SK Hynix |

4.6 |

5.1 |

12% |

Digitimes, April 2015 |

|||

Global Foundries |

4.8 |

4.8 |

0% |

$9B-10B in 2014 through 2015 |

|||

Micron Technology |

1.3 |

3.8 |

186% |

Fiscal year ending August |

|||

Flash Ventures |

1.4 |

2.0 |

43% |

SC IQ, Apr. 2015 |

|||

UMC |

1.4 |

1.8 |

29% |

||||

SMIC |

1.0 |

1.4 |

38% |

||||

Infineon |

0.9 |

0.9 |

4% |

SC IQ, Apr. 2015 |

|||

STMicroelectronics |

0.5 |

0.5 |

7% |

SC IQ, Apr. 2015 |

|||

Texas Instruments |

0.4 |

0.5 |

30% |

SC IQ, Apr. 2015 |

|||

NXP Semiconductors |

0.3 |

0.4 |

6% |

SC IQ, Apr. 2015 |

|||

Total of above |

49.5 |

55.7 |

12% |

||||

Total Industry |

65.0 |

69.0 |

6% |

IC Insights, Jan. 2015 |

|||

Others |

15.5 |

13.3 |

-14% |

||||

Overall the listed companies are expected to total $55.7 billion in 2015 capex, up 12% from 2014. Based on IC Insights forecast of $69.0 billion for the total semiconductor industry, this leaves $13.3 billion for other companies, down 14%. Eight of the nine biggest spenders are either memory companies or foundries. Flash Ventures is a combination of manufacturing joint ventures between Toshiba and SanDisk which account for most of their memory supply. Four of the companies on the list (Infineon Technologies, STMicroelectronics, Texas Instruments and NXP Semiconductor) are top 15 semiconductor suppliers which once depended primarily on internal wafer fabs. These companies are increasing their reliance on foundries and thus their capex is now rather small relative to their sales. The “others” category largely consists of small to medium size companies producing analog and discrete semiconductors.

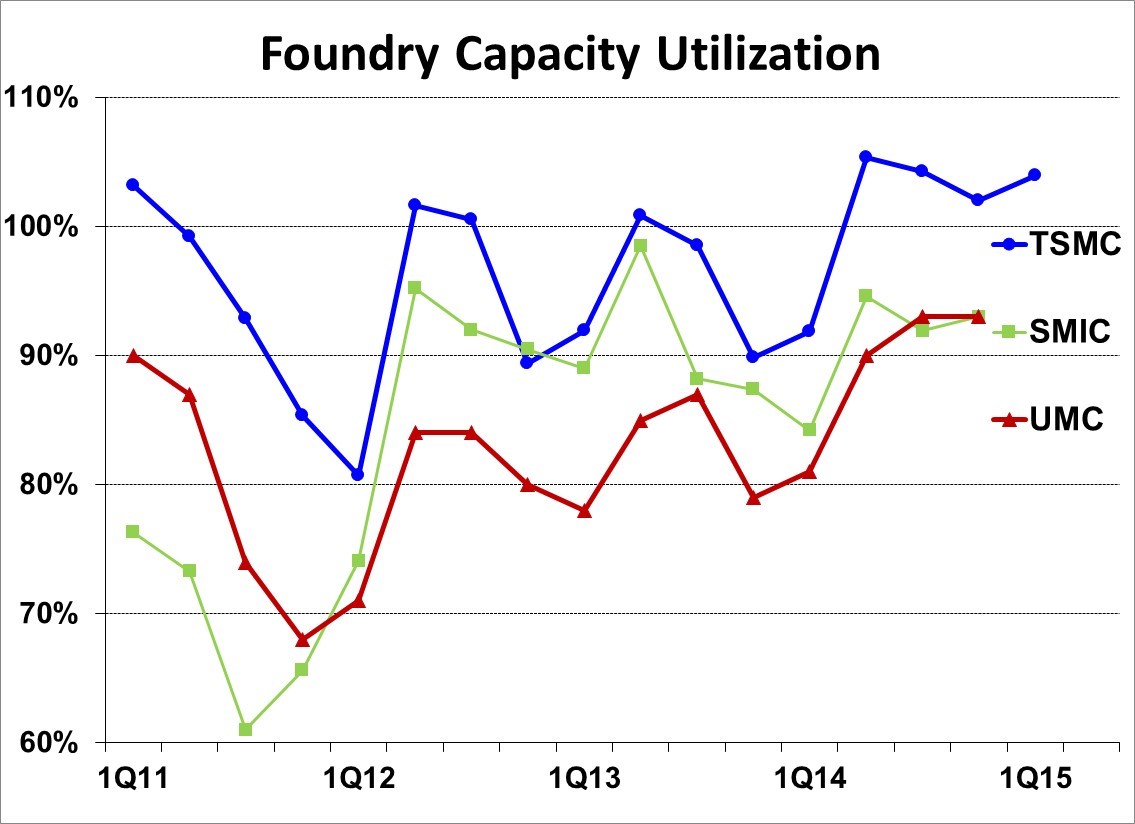

Do current industry conditions justify the strong increase in capex by the foundry companies? TSMC, UMC and SMIC combined are expected to increase their capex 17% in 2015. Global Foundries expects $9 billion to $10 billion in capex in 2014 and 2015 combined, but did not indicate the amount each year. The capacity utilization trends of TSMC, SMIC and UMC show high utilization rates since second quarter 2014 after dips in late 2013. TSMC does not report a utilization rate. The TSMC utilization calculated by dividing wafers shipped by wafer capacity results in unrealistic rates above 100%. However the calculated number provides a general trend in TSMC’s utilization.

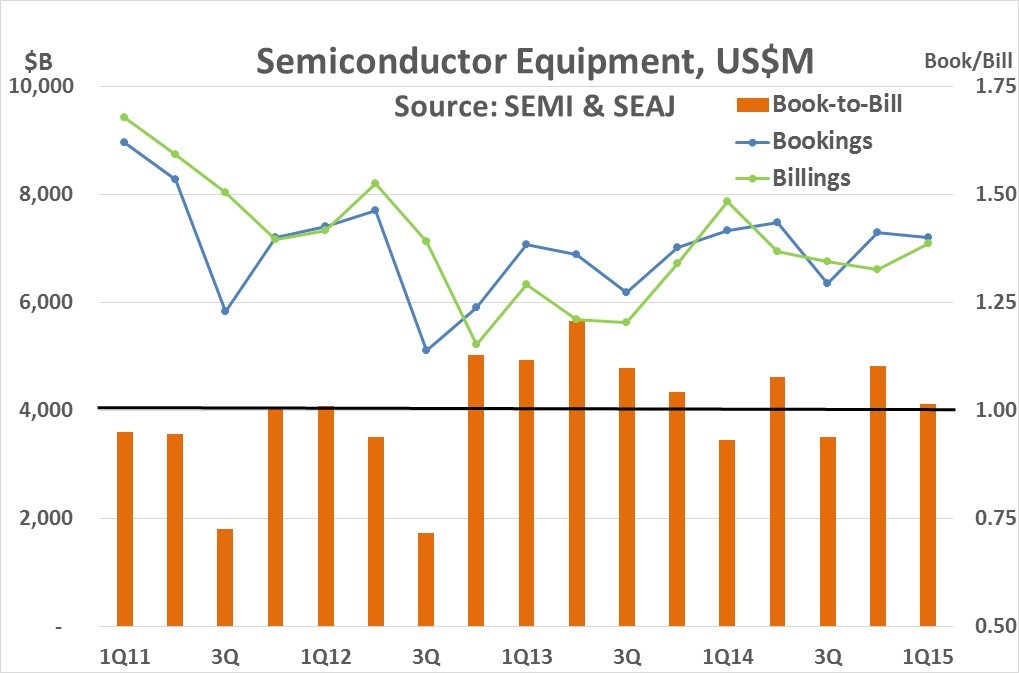

Bookings and billings for semiconductor manufacturing equipment show a relatively healthy market, based on data from SEMI and SEAJ. Although billings have been relatively flat for the last four quarters, the book-to-bill ratio has been above 1.0 for the last two quarters indicating near term growth.

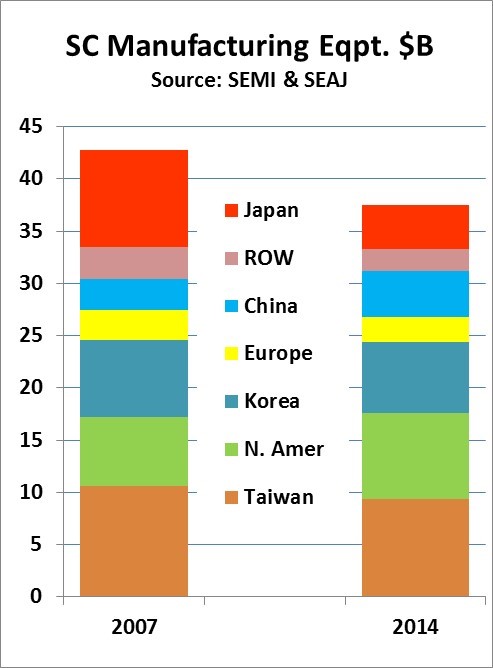

2014 semiconductor manufacturing equipment shipments were $37.5 billion, up 18% from 2013. Shipments were still well below the $43.5 billion in 2011 and the $42.8 billion in 2007, before the last major semiconductor downturn. The chart below shows shipments by region for 2007 and 2014. Shipments in 2014 were $5.3 billion lower than 2007. The difference is primarily in Japan, which was $5.1 billion lower. Shipments were higher in 2014 in North America (up 25%) and China (up 50%). Shipments were lower in South Korea, Taiwan, and the rest of the world (ROW).

2015 should be a good year for semiconductor capital expenditures and semiconductor manufacturing equipment. However it is dependent on continuing healthy demand for semiconductors. Our latest forecast at Semiconductor Intelligence is for 8% semiconductor market growth in 2015, enough to support the current capex outlook.