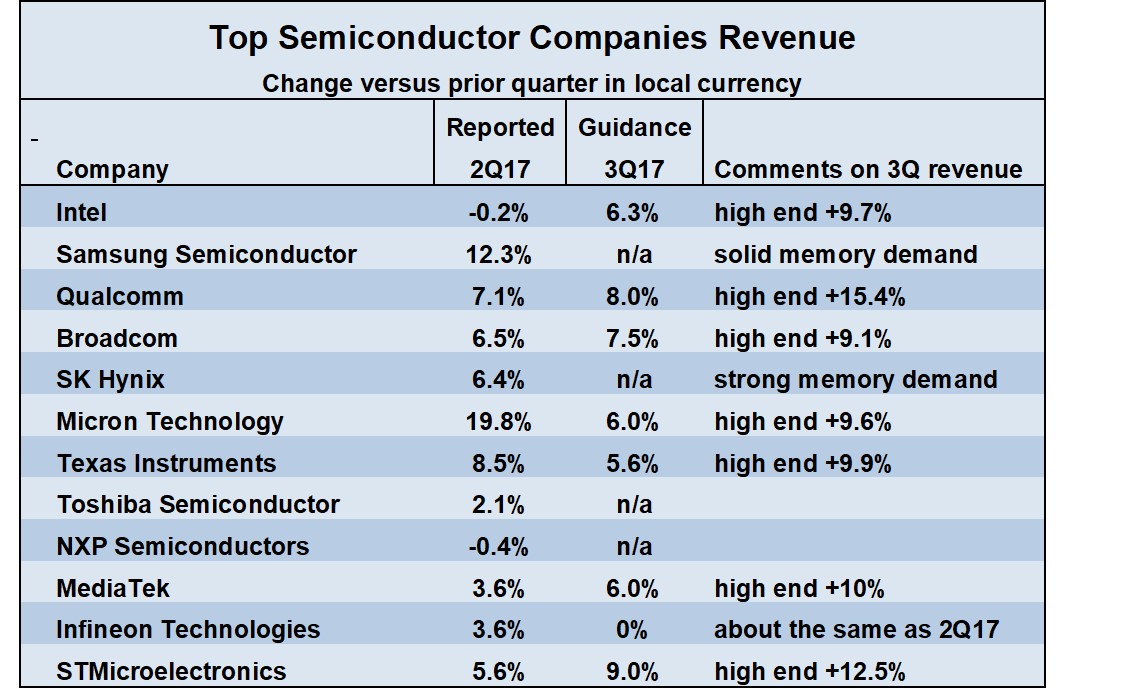

The 2017 semiconductor market is shaping up as the strongest since 2010 – when the market grew 32% as it bounced back from the 2008-2009 downturn. According to World Semiconductor Trades Statistics (WSTS), the second quarter 2017 semiconductor market was up 5.8% from 1Q 2017 and up 23.7% from a year ago. Much of the market vitality is due to memory – specifically DRAM and NAND flash. This is illustrated by quarter-to-quarter revenue change of the major memory companies. Samsung revenues (in Korean won) were up 12.3% in 2Q17 versus 1Q17. Micron Technology revenues were up 19.8%. SK Hynix revenues (in Korean won) were up 6.4% in 2Q17, following 17.4% growth in 1Q17. Company guidance for 3Q17 shows continued strength in memory. Micron guided for 6.0% growth in 3Q17, with high-end guidance of 9.9%. Samsung and SK Hynix did not provide 3Q17 guidance, but both companies expect continued strong demand for DRAM and NAND flash. Micron expects healthy memory demand to continue into 2018.

A good sign of the health of the overall semiconductor market is the 3Q17 outlook for non-memory companies. Most of the major non-memory companies expect 3Q17 revenue to increase in the range of 5.6% to 9.0%. The exception is Infineon, which guided for 3Q17 revenue to be about the same as 2Q17. The high end of guidance from the non-memory companies shows the potential for close to double-digit growth. Excluding Infineon, the high end guidance ranges from 9.1% from Broadcom to 15.4% from Qualcomm.

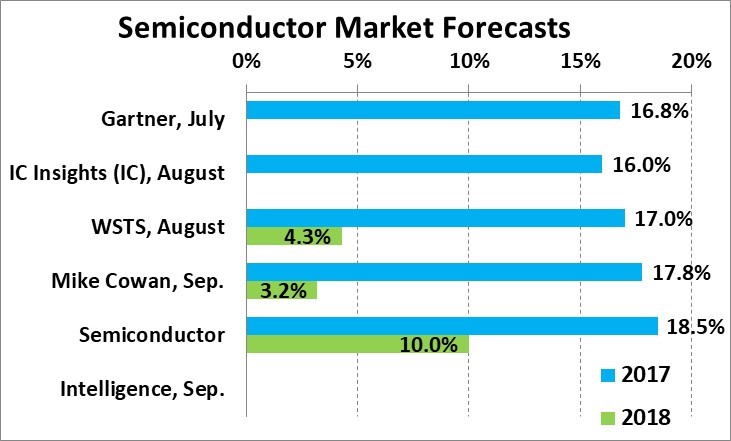

Recent forecasts for the semiconductor market reflect this strength. WSTS’s June projection was 11.5% growth in 2017. In August, WSTS revised its forecast based on final 2Q 2017 data to 17.0%. Other recent forecasts range from 16% (for the IC market) from IC Insights to our Semiconductor Intelligence updated projection of 18.5%.

The available forecasts for 2018 generally call for a significant slowdown in the semiconductor market. WSTS expects 4.3% change and Mike Cowan’s latest projection is for 3.2% change. Our updated outlook at Semiconductor Intelligence is 10.0% growth in 2018. Our higher number is based on several key assumptions:

- No crash in the memory market. The current boom in the DRAM and NAND flash markets is largely driven by increasing prices. This is not sustainable. Eventually supply and demand will move toward a balance – through an increase in supply as more capacity is added; through a decrease in demand as end equipment markets slow; or through a combination of the two. The memory market has seen major downturns in the past when demand from end equipment makers has declined significantly. As demand fell off, memory companies cut prices in an effort to keep fabs running. We do not expect any falloff in demand in 2018. The DRAM and NAND flash markets should experience a moderate correction, but not a significant decline.

- Strong quarterly pattern set in 2017. The semiconductor market grew 5.8% in 2Q17 and should experience similar or stronger growth in 3Q17. Thus even moderate quarter-to-quarter growth in 2018 can lead to an annual increase close to double digits.

- Continued electronic equipment growth. The major drivers of semiconductor demand have been PCs, tablets and mobile phones. Although these markets have been sluggish in the last few years, Gartner expects 2018 to improve over 2017. Automotive is becoming a significant market for semiconductors. Gartner projects growth in this market will pick up from 6% in 2017 to 7% in 2018. Semiconductors for Internet of Things (IoT) applications is an emerging market. IC Insights forecasts healthy IoT SC growth of 16% in 2017 and 15% in 2018. The global economy should see a slight pickup from 3.5% growth in 2017 to 3.6% in 2018, according to the International Monetary Fund (IMF).