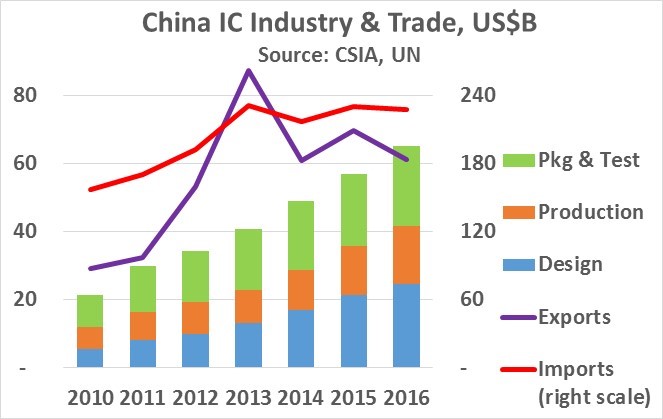

China has long been the largest market for semiconductors, accounting for over 50% of the global market for the last five years. China is now on track to become the largest semiconductor manufacturer in the next few years. The chart below shows China’s integrated circuit (IC) industry from 2010 to 2016, according to the China Semiconductor Industry Association (CSIA). The chart also shows China IC exports (purple line on left scale) and IC imports (red line on right scale), based on United Nations (UN) trade data. China IC imports surged 47% from $157 billion in 2010 to $231 billion in 2013. However, since 2013 imports have been flat in the $218 billion to $231 billion range. China IC exports tripled from $29 billion in 2010 to $88 billion in 2013. In the last three years, exports have dropped back to the $61 billion to $70 billion range.

China’s domestic IC industry has exploded over the last six years, tripling in size from $21 billion in 2010 to $65 billion in 2016. The fastest growing segment has been IC design, increasing 5 times from $5 billion in 2010 to $25 billion in 2016. The data shows China is increasingly furnishing its IC needs internally, become less dependent on non-Chinese IC companies.

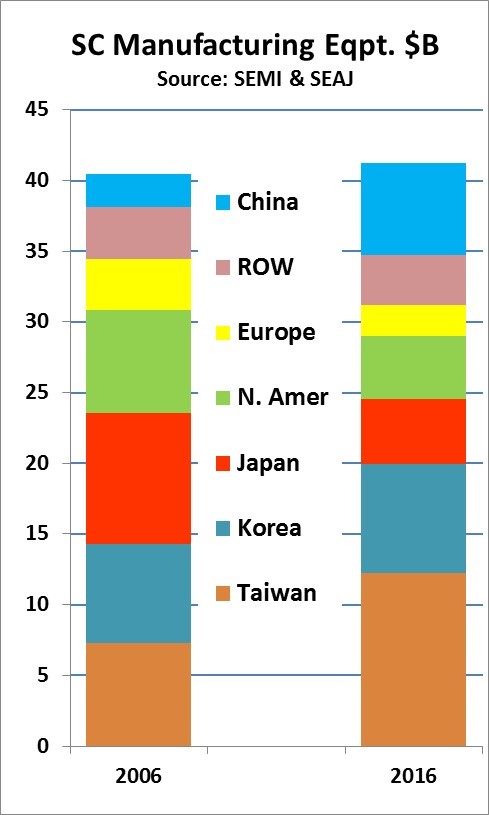

China’s growing production of semiconductors is reflected by wafer fab equipment spending trends over the last ten years. According to data from SEMI and SEAJ, China purchases of fab equipment grew 180% from $2.3 billion in 2006 to $6.5 billion in 2016. Over the same period, fab equipment purchases declined 50% in Japan and 39% in both North America and Europe. South Korea grew 10% and Taiwan grew 67%. In 2016 China trailed behind Taiwan at $12.2 billion and South Korea at $7.7 billion. However, SEMI expects China will be the largest fab equipment market by 2019.

At the SEMI China conference last week, ASE Group COO Tien Wu predicted China’s fabless IC design industry will account for over 40% of the global fabless IC revenue in the near future. According to Digitimes, he also projected China’s wafer foundry industry will be 25% of the global market and Chinese integrated device manufacturers (IDMs) will be 20%.

China’s growth in wafer foundry services is reflected by the capital spending of Semiconductor Manufacturing International Corporation (SMIC). According to IC Insights, SMIC’s capital spending was $2.6 billion in 2016, up 87% from 2015 and the fastest growth rate of the top eleven spenders. IC Insights forecasts SMIC capital spending of $2.3 billion in 2017. While this is less than a quarter of the spending projected for foundry giant TSMC, it is more than the $2.0 billion each of the second and third largest foundries, GlobalFoundries and UMC.

In our January newsletter, we explained how Chinese electronics companies were moving from just assembly to fully integrated companies including design, marketing and sales. Thus China’s electronics industry is becoming less dependent on foreign electronics companies. In the same manner, China’s developing semiconductor industry will make the nation less dependent on foreign semiconductor companies. Chinese semiconductor companies will increasingly design and manufacture devices to support Chinese electronics companies. Eventually, the Chinese semiconductor companies will be serious competitors for business outside of China.