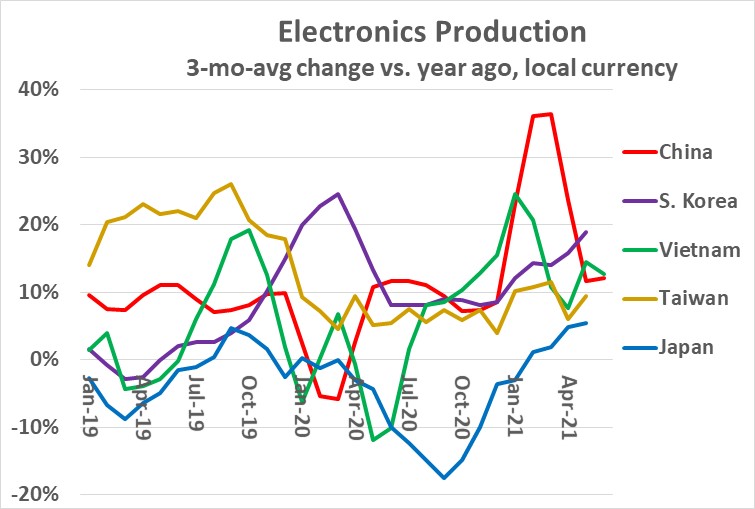

Electronics production continues to recover from the COVID-19 pandemic. However, the recovery is mixed by country. The chart below shows three-month-average (3/12) change versus a year ago in electronics production by local currency for key Asian countries. China was averaging about 10% growth prior to the pandemic. After a sharp drop in early 2020, China recovered to about 10% growth. June 2021 3/12 growth was 12%. South Korea electronics production was largely unaffected by the pandemic. 3/12 growth never dropped below 8% in 2020 and was a strong 19% in May 2021. Taiwan also experienced minimal disruption, with 3/12 change above 4% in each month of 2020. Taiwan 3/12 change has averaged about 10% in 2021. Vietnam had pandemic related fluctuations in 2020 but bounced back to 13% 3/12 growth in June 2021. Japan electronics production has been weak for several years. 3/12 change dropped to negative 18% in September 2020. Japan recovered to 5% 3/12 growth in May 2021.

The United States and Europe had more COVID-19 cases relative to their population than the Asian countries, according to the World Health Organization (WHO). The U.S. and Europe each had over 100 COVID-19 deaths per 100,000 people. Most major Asian countries had fewer than 10 COVID-19 deaths per 100,000 people. Some exceptions were India at 30, Malaysia at 22 and Japan at 12.

Despite the relatively high number of COVID-19 cases and deaths, U.S. electronics production did not experience a significant slowdown. U.S. 3/12 change in 2020 never dropped below a 1% decline. Production for the year 2020 was up 3.6% from 2019, the highest annual growth since 2008. 2021 3/12 change has been about 8% each month, with May up 9%.

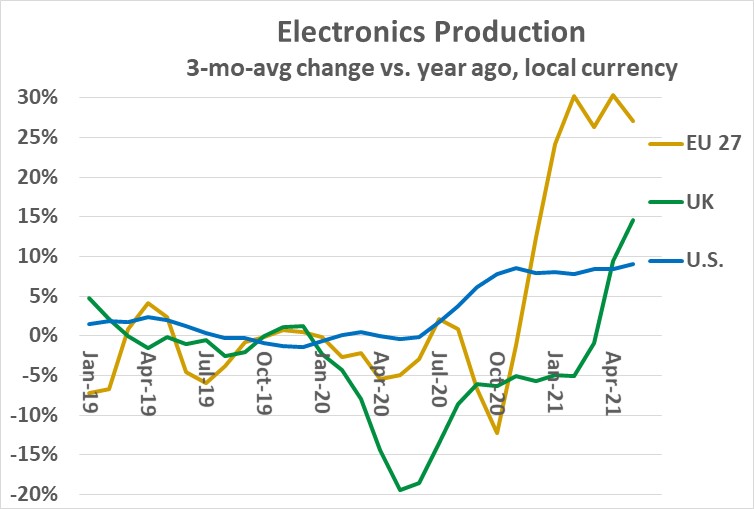

The United Kingdom (UK) officially withdrew from the European Union (EU) in January 2020 in a process known as Brexit. Thus, Europe had to deal with the effects of Brexit as well as COVID-19. The 27 EU countries (EU 27) have shown strong 3/12 growth of over 24% in each month of 2021 after declines in most months of 2020. UK electronics production had 3/12 declines in every month of 2020, with the worsts months in May and June at a 19% decline. The UK has recovered in the last few months, with May 2021 3/12 growth of 15%.

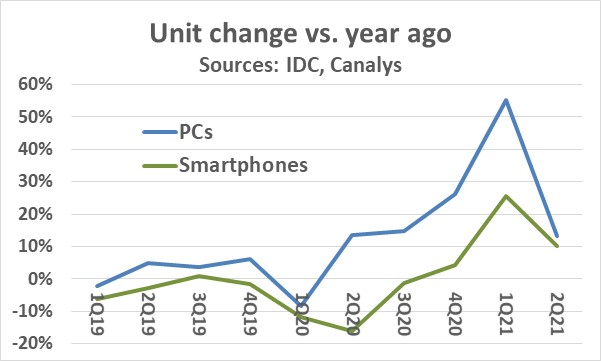

Two key electronic products are PCs and smartphones. These are relatively mature products with flat to declining unit shipments over the last few years. However, these products experienced totally different trends during the pandemic. Based on data from IDC, smartphone units versus a year ago declined 12% in 1Q 2020 and 16% in 2Q 2020 primarily due pandemic-related production cuts in China. Smartphone units recovered to 26% year-to-year growth in 1Q 2021. Estimates based on Canalys data in 2Q 2021 show 10% growth versus a year ago. Smartphone units declined 5.8% in the year 2020 versus 2019. In May 2021 IDC forecasted 7.7% growth for smartphone units in 2021, slowing to 3.8% growth in 2022.

PC unit shipments had an entirely different trend. IDC data shows 1Q 2020 units declined 8% from a year ago, largely due to pandemic related supply issues. PCs bounced back robustly with 2Q 2020 up 14% year on year. Growth has been above 10% since, with 2Q 2021 up 13%. For the year 2020, PC units were up 12%, the strongest annual growth in ten years. PC demand has been driven by pandemic trends. Many countries had stay-at-home orders or recommendations for several months of 2020. People had to rely on PCs connected to the internet for work, education, and entertainment. Many households without PCs acquired them, often paid for, or subsidized by, employers or school systems. Many households with PCs upgraded with new models and/or added additional units. IDC expects strong PC growth to continue in 2021, with their May 2021 forecast for 18% growth. IDC expects the PC market to correct in 2022 with a 3% decline.

To understand the effects of the pandemic on the electronics industry, it is helpful to compare data for 2021 to the pre-pandemic levels in 2019. Other factors in addition to the pandemic contributed to these trends. Continuing trade friction between China and the U.S. led to some production shifting out of China to other Asian countries. Brexit affected electronics production in the UK versus the EU.

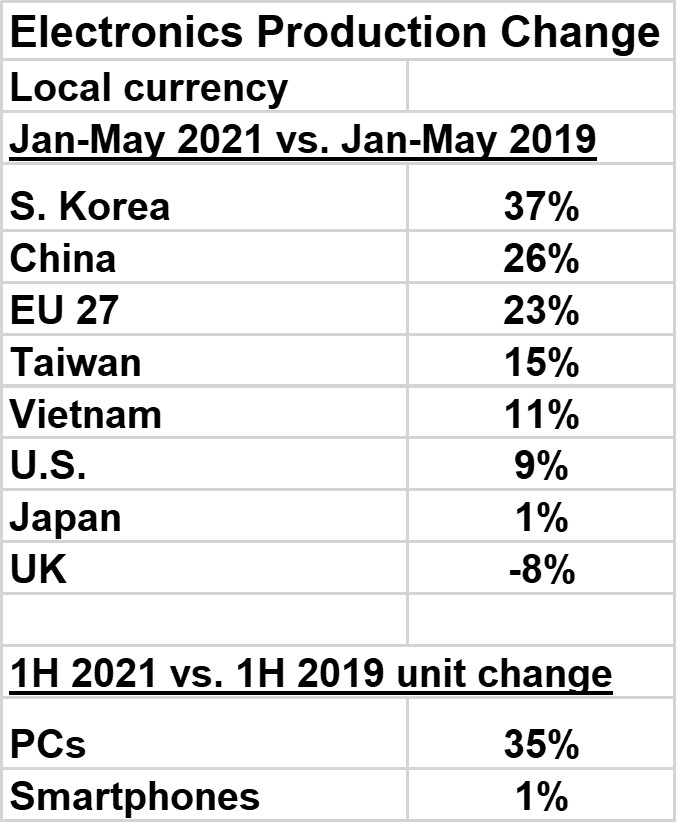

The most substantial change in electronics production for January through May of 2021 compared to the same period in 2019 was in South Korea, up 37%. South Korea saw little disruption in electronics production due to the pandemic. It also benefited from some production shifting from China to South Korea. China was up 26%, as it quickly recovered from pandemic related slowdowns in early 2020. Taiwan was up 15% and Vietnam was up 11% as both countries had relatively minor pandemic-related production disruptions and both benefited from production shifts from China. Japan was up 1%, reflecting its weak electronics production over the last several years.

EU 27 electronics production in January-May 2021 grew 23% versus two years ago, while the UK declined 8%. This likely reflects some Brexit-related production shifts from the UK to the EU countries. The U.S. was up 9%, the strongest growth in over a decade. Despite relatively high COVID-19 rates in the U.S., electronics production was largely unaffected. This is likely due to highly automated production in the U.S. compared to labor intensive production in China and other countries.

The difference in the PC and smartphone markets is highlighted by comparing units shipped in the first half of 2021 compared to the first half of 2019. PCs were up 35% while smartphones were only up 1%.

The COVID-19 pandemic is far from over, with WHO showing rising cases and deaths in the last several weeks. However, the major disruptions to society and industry are mostly over. The electronics industry is generally back on track.