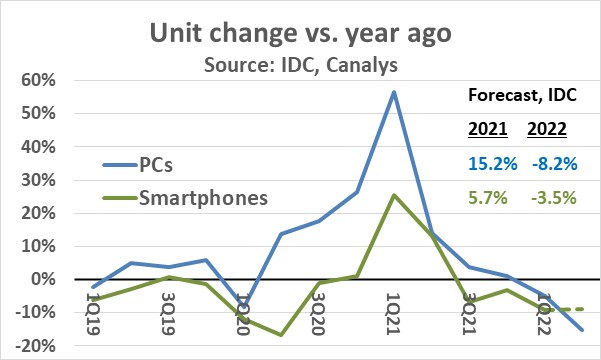

Key semiconductor market drivers PCs and smartphones are both showing declines in shipments in the first half of 2022. According to IDC, PC shipments in 2Q 2022 were down 15% from a year earlier. 2Q 2022 PC shipments of 71.3 million units were at the lowest level in almost three years since 70.9 million units were shipped in 3Q 2019. In June, prior to the 2Q 2022 PC shipment data, IDC forecast a decline of 8.2% in PC shipments for the year 2022. Based on the 2Q 2022 data, the forecast will probably be lowered to a double-digit decline.

Smartphone shipments 1Q 2022 were down 9% from a year ago, according to IDC. IDC’s 2Q 2022 smartphone data has not yet been released, but Canalys estimated smartphone shipments were down another 9% in 2Q 2022 versus a year ago. IDC’s June forecast called for a 3.5% decline in smartphone shipments in 2022, but based on 2Q 2022 data the decline should be at least double that rate, in the -7% to -10% range.

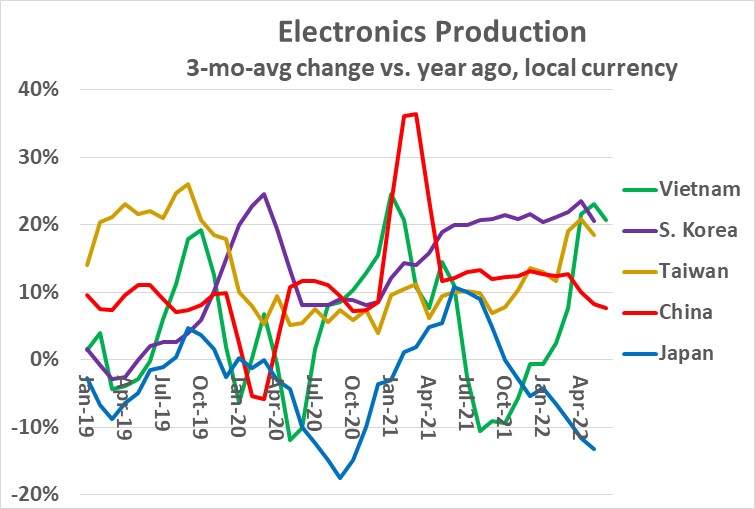

Electronics production in the key Asian countries is mixed. China, the largest producer, showed three-month-average change versus a year ago (3/12) of 7.7% in June, a slowing from double-digit growth from January 2021 through April 2022. Much of the slowdown in China electronics production was due to COVID-19 related shutdowns in April and May. Japan electronics production has been declining since October 2021, with May 2022 3/12 change down 13%. South Korea, Vietnam and Taiwan have shown strong growth in the last few months, with 3/12 change around 20%.

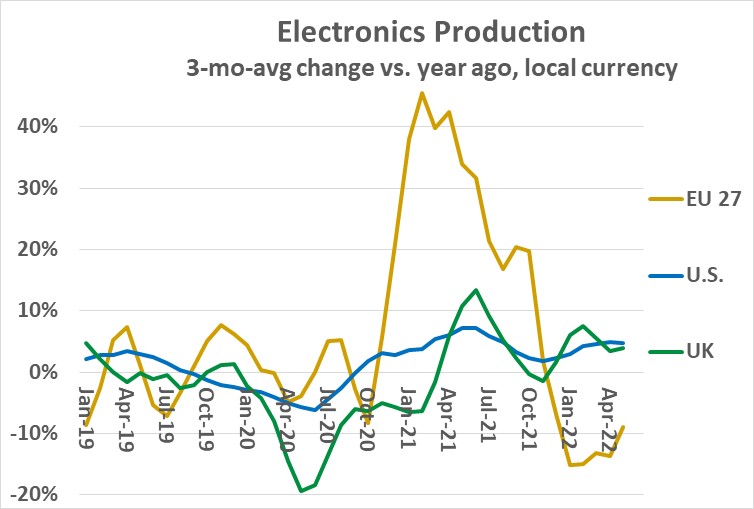

In the U.S and Europe, electronics production trends are also mixed. U.S. 3/12 change was 4.7% in May, in line with the trend over the last year. UK 3/12 change was 4.0% in May, the sixth straight positive month. UK electronics declined significantly in 2020 mostly due to production shifts from the UK to European Union (EU) countries after the UK withdrew from the EU (Brexit). The 27 countries of the EU showed healthy electronic production growth in most of 2021 due to Brexit and recovery from the COVID-19 pandemic. In the last six months, EU 27 3/12 change has been negative, with a 9% decline in May.

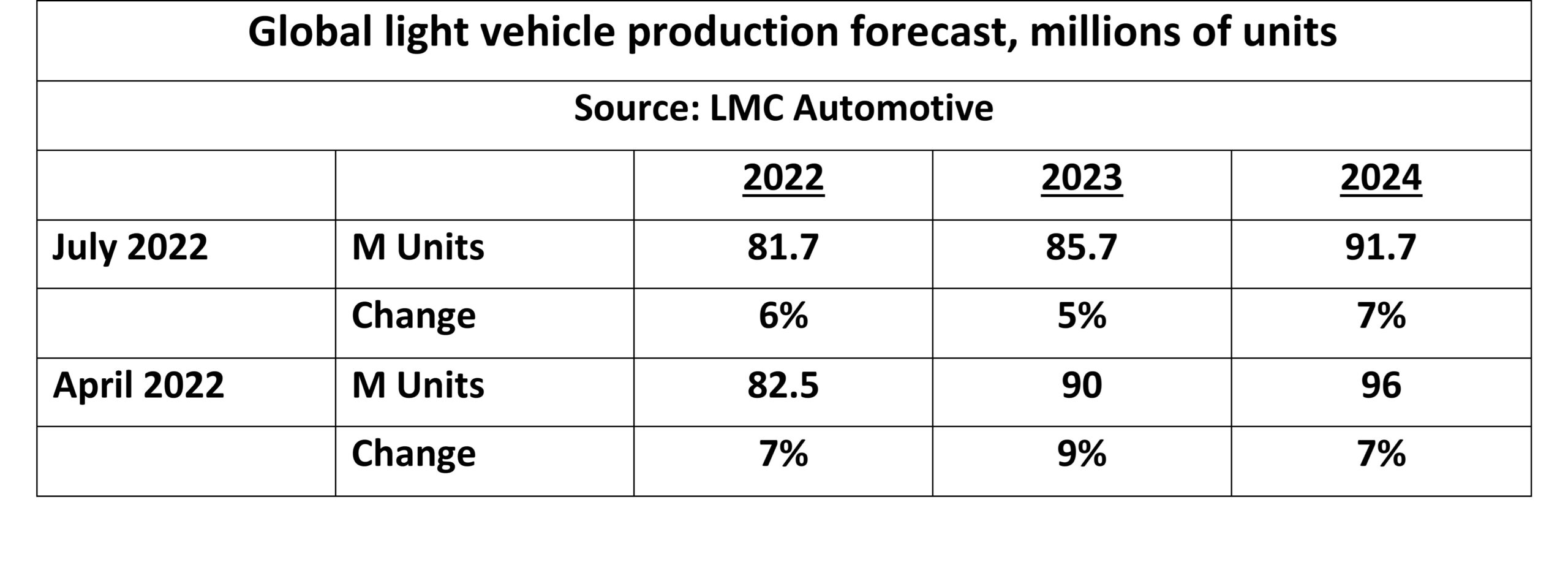

The bright spot for the semiconductor market is the automotive sector. LMC Automotive’s forecast for 2022 light vehicle production is 81.7 million units, up 6% from 2021. LMC projects growth of 5% in 2023 and 7% in 2024. However, the July numbers have been revised downward from the April forecast by 0.8 million in 2022 and 4 million in both 2023 and 2024. The downward revisions were due to continued shortages of semiconductors and other components, the China lockdown in April and May, the war in Ukraine, and worries over inflation and interest rates.

The overall outlook for electronics production is uncertain. Most countries are showing growth in production, with the exceptions of Japan and the EU. However, declines in shipments of PCs and smartphones are a cause for concern. Although automotive production is growing, growth may be limited by the factors listed above. A global recession in 2023 is increasingly likely. The International Monetary Fund (IMF) puts the chance of a recession at 15%. Citigroup and Deutsche Bank each see about a 50% chance. A Wall Street Journal survey of economists has the risk of a U.S. recession at 44%. The semiconductor industry needs to exercise caution in light of these factors.

The overall outlook for electronics production is uncertain. Most countries are showing growth in production, with the exceptions of Japan and the EU. However, declines in shipments of PCs and smartphones are a cause for concern. Although automotive production is growing, growth may be limited by the factors listed above. A global recession in 2023 is increasingly likely. The International Monetary Fund (IMF) puts the chance of a recession at 15%. Citigroup and Deutsche Bank each see about a 50% chance. A Wall Street Journal survey of economists has the risk of a U.S. recession at 44%. The semiconductor industry needs to exercise caution in light of these factors.