SEMICON Southeast Asia was held this week in Penang, Malaysia. Over 6500 people attended the conference to learn about the latest trends and equipment in semiconductor manufacturing.

Dr. Dan Tracy, Senior Director Industry Research and Statistics at SEMI, presented an optimistic outlook for the semiconductor equipment market in 2017. Semiconductor capital spending (cap ex) and semiconductor manufacturing equipment spending are both expected to show double digit growth, with cap ex at 10.9% and equipment at 12.2%.

Semiconductor Capital Spending & Manufacturing Equipment ForecastAnnual Change, Source: SEMI April 2017 |

|||

2015 |

2016 |

2017 |

|

CapEx |

-0.5% |

3.8% |

10.9% |

Equipment |

-2.6% |

12.9% |

12.2% |

The strong growth is driven by key semiconductor applications: storage, industrial, wireless, automotive and consumer. The strongest growth in semiconductor products will be in memory (up 15% to 20%) and sensors (up 9% to 11%).

China will be the major source of growth in semiconductor manufacturing over the next few years according to Clark Tseng, senior research manager of SEMI Taiwan. China has 20 new wafer fabs started or planned from 2016 to 2019 and is expected to account for 20% of global wafer fab capacity by 2020. Foreign companies have accounted for the majority of wafer fab spending in China, but Chinese companies should account for the majority of spending by 2018. China should be the largest market for wafer fab equipment by 2019 or 2020.

Lung Chu, president of SEMI China, discussed the Chinese government’s commitment of about US$75 billion to expand the semiconductor industry in China. The key reasons China wishes to expand its semiconductor industry are:

-

Reduce the annual semiconductor trade deficit of over $160 billion, the largest for any product category including oil.

-

Ensure domestic production of semiconductors needed for national security.

-

Increase participation in the industry driving innovation in electronics.

According to Lung Chu, China has some hurdles to overcome to catch up to the rest of the world. China fabless semiconductor companies are weak in microprocessors, microcontrollers, FPGAs, DSPs and memory. Chinese foundries are about two generations behind the major foundries in process technology.

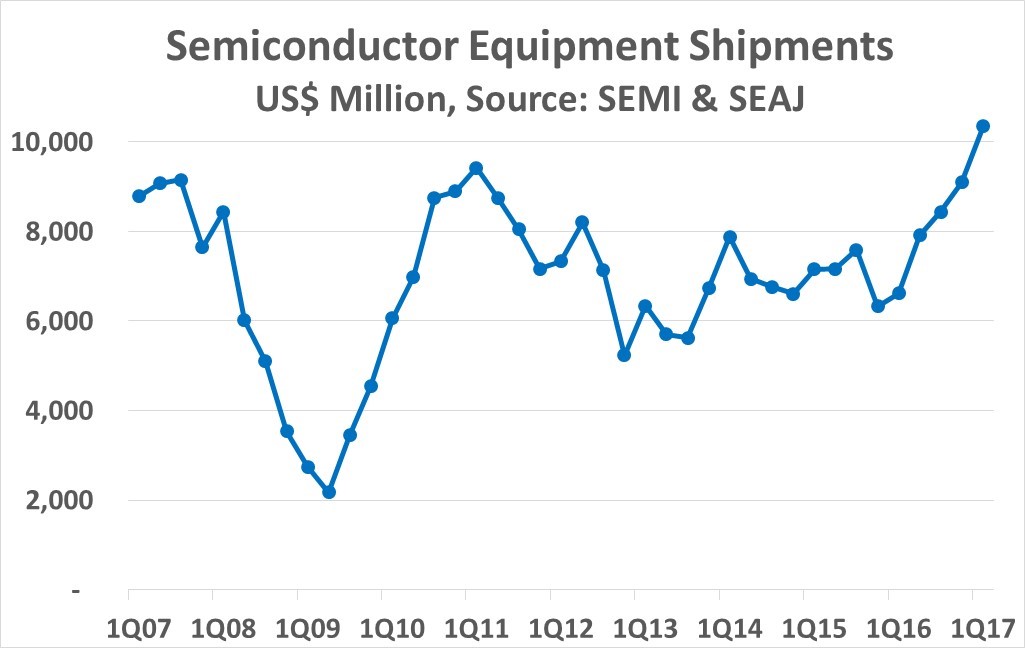

1Q 2017 equipment market up 57% yr/yr

SEMI’s optimism semiconductor manufacturing equipment growth in 2017 supported by the combined shipment data from SEMI and SEAJ. 1st quarter 2017 shipments were $10,360 million, up 14% from 4Q 2016 and up 57% from a year ago. SEMI discontinued bookings data in December 2016, when the book-to-bill ratio was 1.06. SEAJ’s book-to-bill ratio in March 2017 was 1.12. We at Semiconductor Intelligence are projecting full year 2017 equipment growth will be in the 30% to 40% range.

The $10 billion quarterly level for semiconductor manufacturing equipment has not be reached since the boom year of 2000. The five quarters of consecutive quarter-to-quarter growth has also not been seen since 2000, except for the 2nd half 2009 to 2010 recovery from the 2008 to 1st half 2009 downturn.

Is the current boom in semiconductor manufacturing equipment driven by real need for additional capacity or could the industry be headed for overcapacity? It is too early to tell; however, the 2017 capital spending plans of major semiconductor companies provide a clue. IC Insights in March projected total cap ex in 2017 of $72.3 billion, up 6% from 2016. The top ten spenders account for 77% of the total.

2017 Capital Spending Forecast, US$B |

||||

Sources: IC Insights, March 2017; Semiconductor Intelligence, April 2017 |

||||

|

|

2016 |

2017 |

Change, $B |

% Change |

Memory |

25.8 |

27.2 |

1.4 |

5.3% |

Foundry |

17.2 |

16.3 |

(0.9) |

-5.3% |

Intel |

9.6 |

12.0 |

2.4 |

25% |

Others |

15.3 |

16.8 |

1.5 |

9.8% |

Total |

68.0 |

72.3 |

4.3 |

6.4% |

Memory: Samsung, SK Hynix, Micron, Toshiba, SanDisk/WD |

||||

Foundry: TSMC, SMIC, UMC, GlobalFoundries |

||||

Based on the IC Insights data, we have grouped the top ten spenders by category. The memory companies combined plan a $1.4 billion increase in cap ex, up 5.3%. The foundry companies plan a $0.9 billion decrease, down 5.3%. Intel plans a $2.4 billion increase, up 25%. Intel is in a unique situation, with few significant competitors for its major microprocessor products. The memory companies sell primarily commodity products into a market which is currently booming, with prices almost double a year ago. The foundry companies generally base their capacity plans on the projections provided by their customers. The foundry customers largely sell application specific products and are in close communication with their end customers in their targeted segments.

Thus capital spending growth in 2017 should be largely driven by the memory companies in the middle of a booming commodity market. The foundry companies, arguably closer to the true capacity needs of their customers, are cutting spending. Plans will change over the course of the year. We expect many companies will reduce their planned spending, especially the memory companies. If the current growth in the semiconductor equipment market is based largely on speculation rather than solid demand, we could see a significant correction in 2018 or 2019.