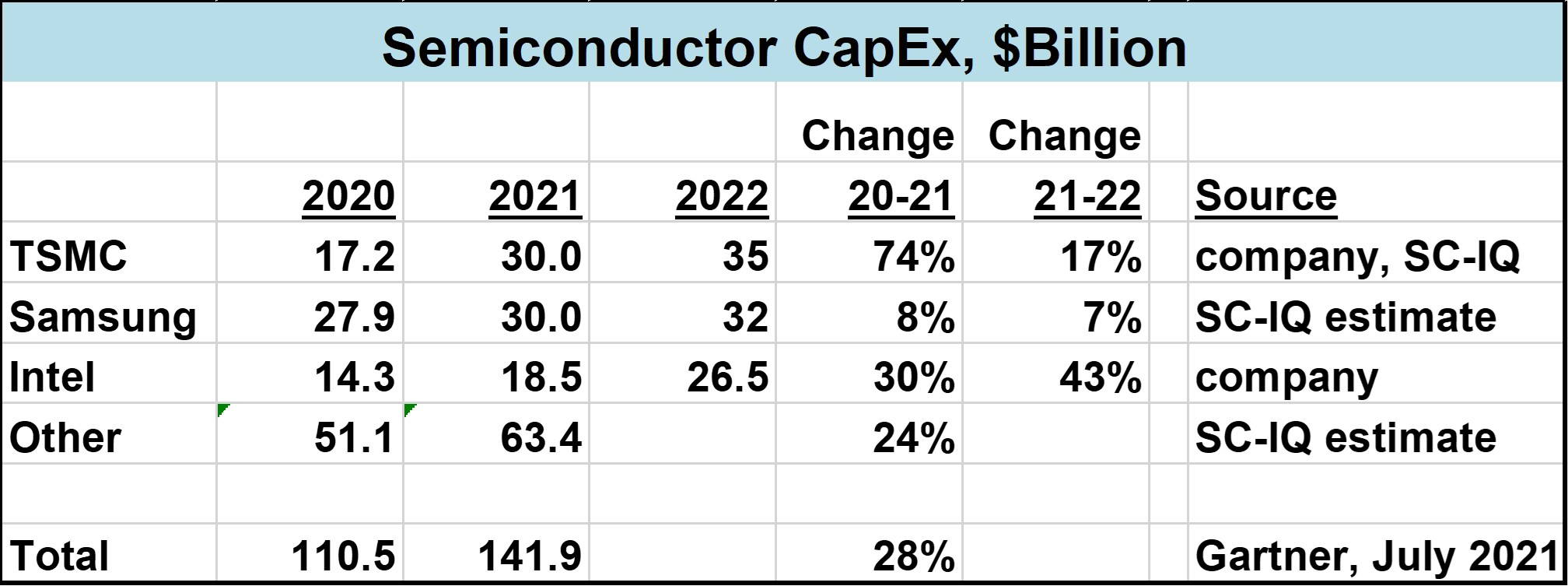

Semiconductor capital expenditures (CapEx) are on track for strong growth in 2021. For many companies the increase should continue into 2022. TSMC, the dominant foundry company, expects to spend $30 billion in CapEx in 2021, a 74% increase from 2020. TSMC announced in March it plans to invest $100 billion over the next three years, primarily for CapEx. Our Semiconductor Intelligence (SC-IQ) estimate is TSMC CapEx will be $35 billion in 2023, but it could go higher.

Samsung is also expected to spend about $30 billion on semiconductor CapEx in 2021. Samsung Group announced a plan to invest 240 trillion won (US$210 billion) over the next three years to expand its businesses. An analyst at Kiwoom Securities in Korea expects about 110 trillion won (US$97 billion) will be semiconductor CapEx. We have estimated Samsung 2022 CapEx at $32 billion, but as with TSMC it could be higher.

Intel surprised analysts in its third quarter 2021 earnings announcement last week with a plan to spend $25 billion to $28 billion on CapEx in 2022, following $18 billion to $19 billion in 2021. Intel will use the funds in an effort to become a major foundry as well as expand and advance capacity for its own products. Based on the mid-point of these ranges, Intel Capex should increase 30% in 2021 and 43% in 2022.

TSMC, Samsung and Intel combined account for over half of total semiconductor industry capital spending. Gartner’s July forecast for 2021 industry CapEx was $141.9 billion, a 28% increase from 2021. Other companies which have projected significant CapEx increases in 2021 include foundries UMC and GlobalFoundries; memory companies Micron Technology and SK Hynix; and integrated device manufacturers (IDMs) STMicroelectronics, Infineon Technologies, and Renesas Electronics.

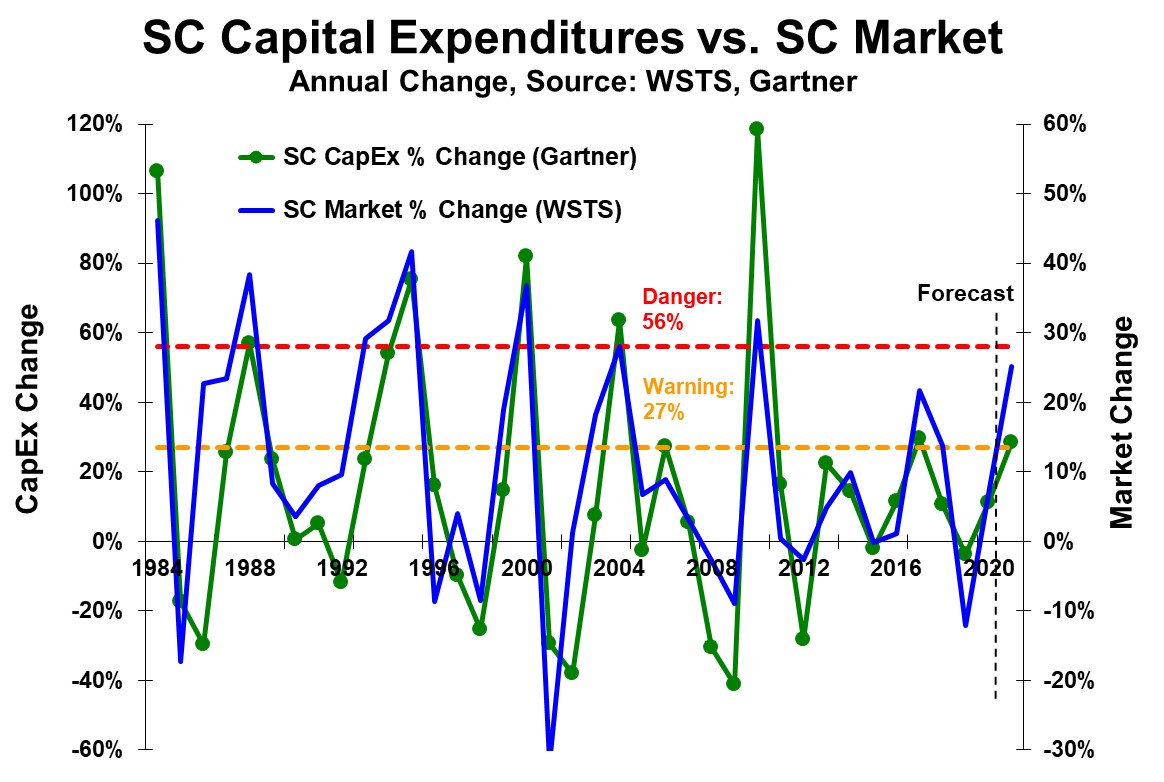

The semiconductor industry is currently experiencing substantial demand improvement from increased automotive electronic content, 5G smartphones and infrastructure, the internet of things (IoT), data centers, and accelerated PC growth due to pandemic-driven home-based work, education, and entertainment. Gartner’s forecast of 28% CapEx growth in 2021 would be the highest since 29% growth in 2017. Should 2021 CapEx grow 30% or more, it will be the highest since 118% in 2010, 11 years ago.

The big question is how much CapEx is too much? The semiconductor industry has a long history of strong CapEx leading to over-capacity followed by price collapses and a declining semiconductor market. The chart below illustrates the relationship between semiconductor CapEx and the semiconductor market. The green line on the left axis is the annual change in CapEx from 1984 through the forecast for 2021. The blue line on the right axis is the annual change in the semiconductor market. Our analysis at semiconductor intelligence has modeled levels of CapEx change which have a major impact on the semiconductor market. The red Danger line is set at 56%. In years when CapEx growth has exceeded 56%, the semiconductor market in the following year has declined or seen a significant deceleration. The orange Warning line is set at 27%. When CapEx growth has been over 27% but less than 56%, the semiconductor market experienced a decline in the next two to three years.

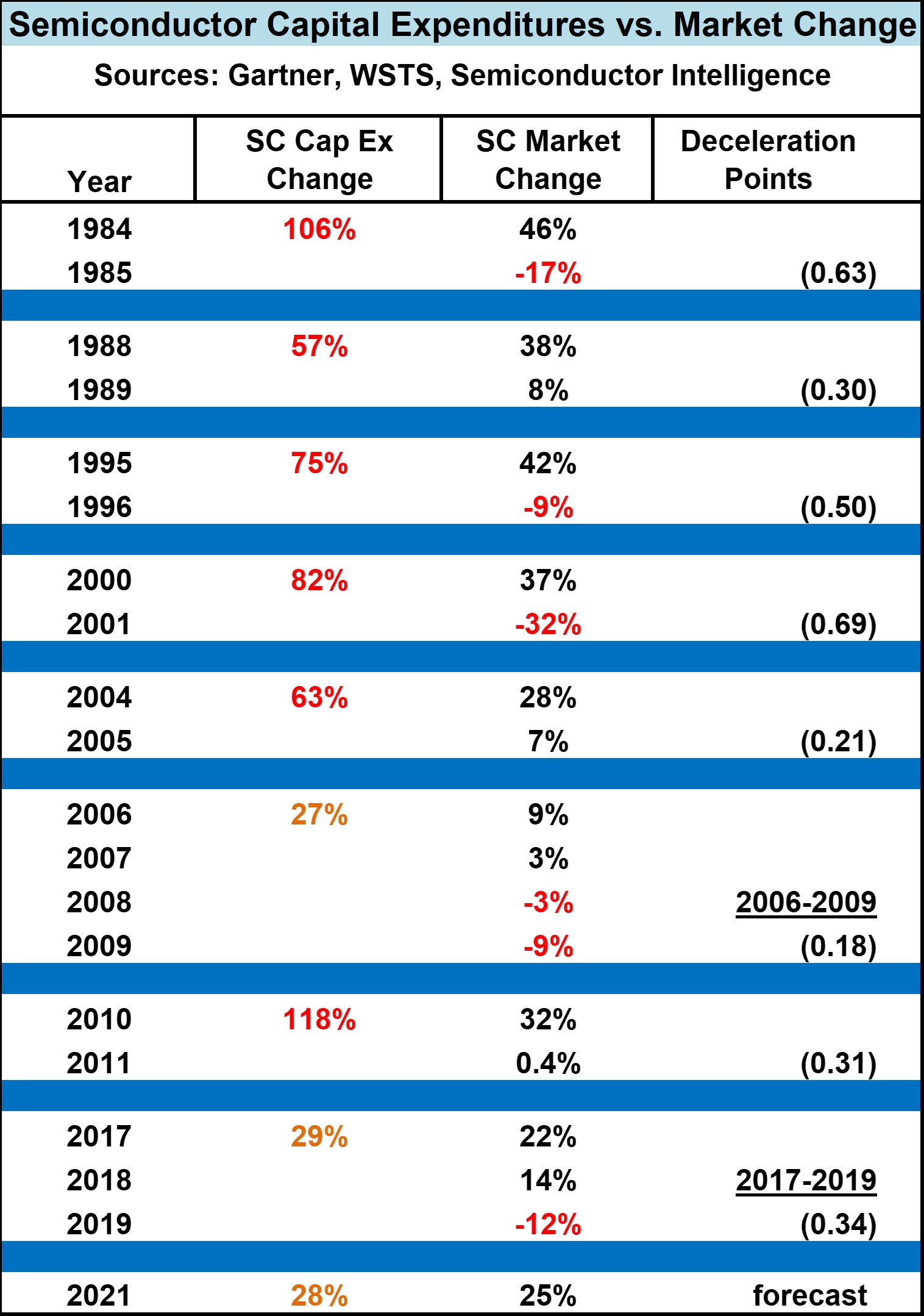

The table below illustrates this process. There have been six years since 1984 where CapEx growth has exceeded 57%. The most extreme cases were in 1984, 1995 and 2000. In 1984, 106% CapEx growth and 46% semiconductor market growth were followed by a 17% market decline in 1985, a growth deceleration of 63 percentage points. In 1995 Capex grew 75% and the market grew 42%. The next year the market declined 9%, a 50-point deceleration. In 2000, 82% CapEx growth and 37% semiconductor market growth was followed by a 2001 decline of 32%, a 69-point growth deceleration. In the three other cases (1988, 2004, and 2010) the market did not decline the following year, but growth decelerated by at least 21 points.

Since 1984 there have been two instances where CapEx growth was greater than 27% but less than 56%. In 2006, CapEx growth was 27% and market growth was 9%. Each of the following three years showed decelerating market increases culminating in a 9% decline in 2009. From 2006 to 2009, growth decelerated a total of 18 points. In 2017, CapEx growth was 29% and market growth was 22%. Over the next two years growth decelerated a total of 34 points, with a 12% decline in 2019.

Gartner’s latest forecast is 28% CapEx growth in 2021 and the WSTS forecast is 25% market growth in 2021. Based on the model above, we should see decelerating growth in the next two to three years, with a possible decline in 2023.

While the model shows consistent trends, the rate of CapEx increases is only one factor affecting semiconductor market growth. High CapEx growth years are usually substantial market growth years, as companies use robust current growth as justification for higher CapEx. The vigorous market rise is usually not sustainable, resulting in major growth deceleration or a decline in the following year. End demand changes also are a major factor in semiconductor market declines. In 1985, the emerging PC market had its first decline. In 2001, the internet bubble burst, leading to a collapse in demand for internet infrastructure and other equipment. In 2017, the smartphone market had its first decline, with declines continuing through 2020.

Although substantial CapEx gains can be a predictor of semiconductor market growth deceleration, it is not necessarily cause and effect. However, strong increases in CapEx bear watching in forecasting the semiconductor market.