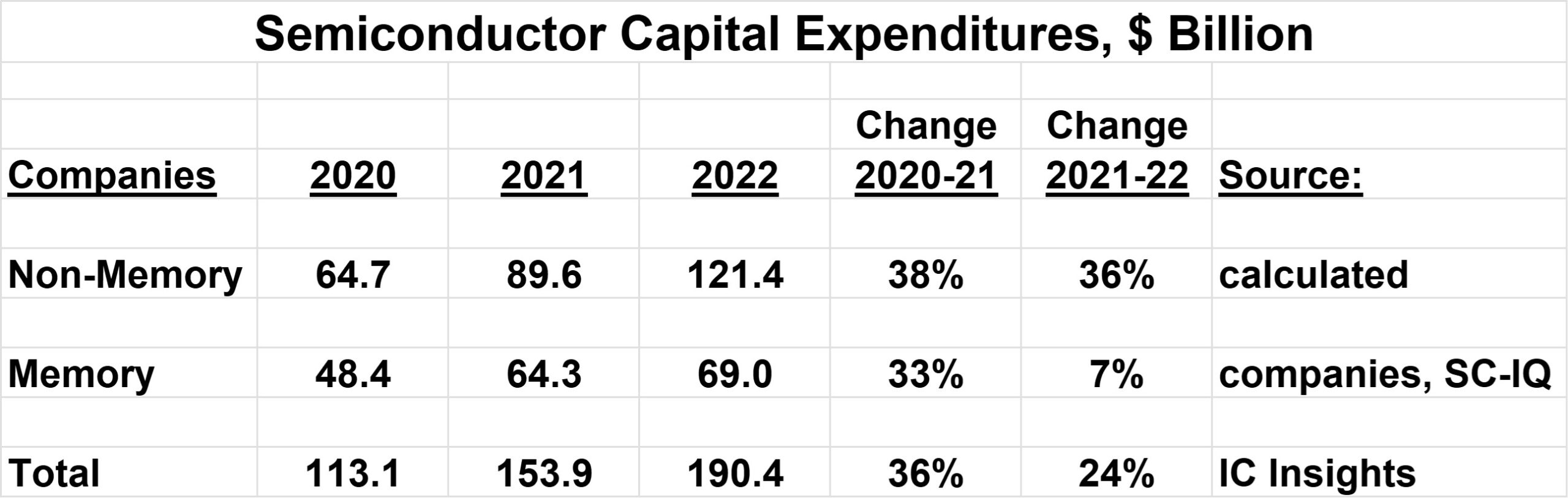

Semiconductor makers are planning strong capital expenditure (CapEx) growth in 2022. According to IC Insights, 13 companies plan to increase CapEx in 2022 by over 40% from 2021. The largest CapEx for 2022 will be from TSMC at $42 billion, up 40%, and Intel at $27 billion, up 44%. IC Insights is forecasting total semiconductor industry CapEx at $190 billion in 2022, up 24% from $154 billion in 2021. 2021 CapEx was up 36% from $113 billion in 2020.

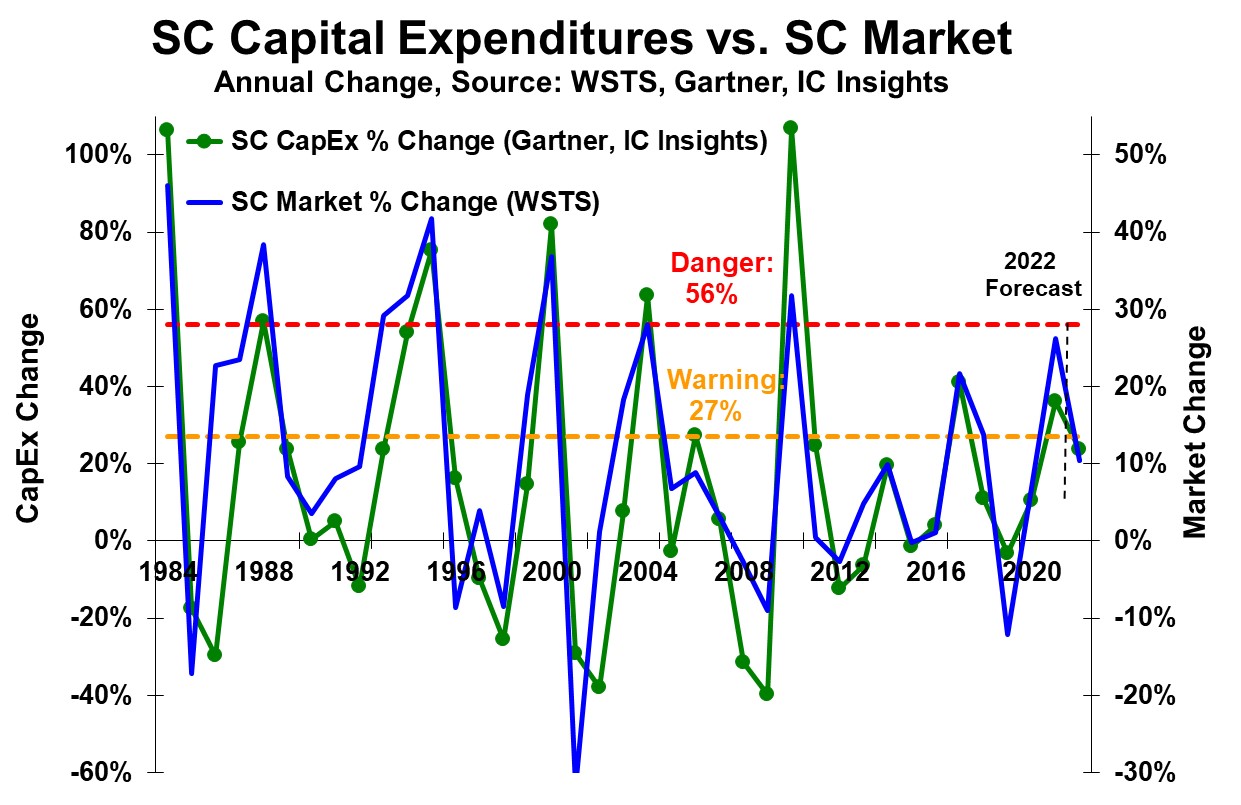

Could this large increase in CapEx lead to overcapacity and a downturn in the semiconductor market? Our analysis at Semiconductor Intelligence has identified points where significant increases in CapEx result in a downturn or significant slowdown in the semiconductor market in the following year or two. The chart below shows the annual change in semiconductor CapEx (green line on the left scale) and the annual change in the semiconductor market (blue line on the right scale). The CapEx data is from Gartner from 1984 to 2007 and from IC Insights from 2008 to 2022. The semiconductor market data is from WSTS. In the last 38 years, semiconductor CapEx growth has exceeded 56% six times (red “danger” line). In each of those six cases, semiconductor market growth has decelerated significantly (greater than 20 percentage points) in the following year. In three of the six cases the market declined the following year. In three of the years from 1984 through 2017, CapEx has exceeded 27% growth (yellow “warning” line) but been less than 56%. In each of these three years (1994, 2006 and 2017) the semiconductor market declined two years later.

2021 CapEx growth of 36% puts it above the warning ling but below the danger line. IC Insights current forecast of 24% CapEx growth in 2022 is close to the warning line. Increases in 2022 CapEx plans could put growth over the 27% warning line but is very unlikely to approach the 56% danger line. So, are we in for a market downturn in 2023?

A few factors may come into play to avoid the overcapacity/downturn cycle this time. Previous large jumps in CapEx have resulted from semiconductor companies chasing fast growing emerging markets. In 1984 it was PCs. In 2000 it was internet infrastructure. In 2010 it was smartphones. In each of these cases, the end market either declined the following year (PCs and internet infrastructure) or slowed (smartphones). In the current situation, semiconductor companies are trying to alleviate shortages, especially in the automotive market. Increasing semiconductor content in vehicles is driving demand for semiconductors. Automotive companies fell behind in semiconductor procurement when they cut production during the pandemic beginning in 2020. In the current case, the demand for automotive semiconductors is not likely to weaken anytime soon.

Another factor is most of the current growth is coming from non-memory companies. In previous cycles, memory companies have been a major driver of CapEx growth. With DRAMs and flash memory primarily commodity products, they are more prone to over-supply and price declines in downturns. In 2021, memory companies grew CapEx 33%, similar to the 38% growth for non-memory companies. In 2022, memory companies are more cautious; we estimate 7% growth in CapEx. With this estimate, non-memory companies CapEx growth would be 36% in 2022. Most of the non-memory products are non-commodity and the companies are more closely linked to their end market customers.

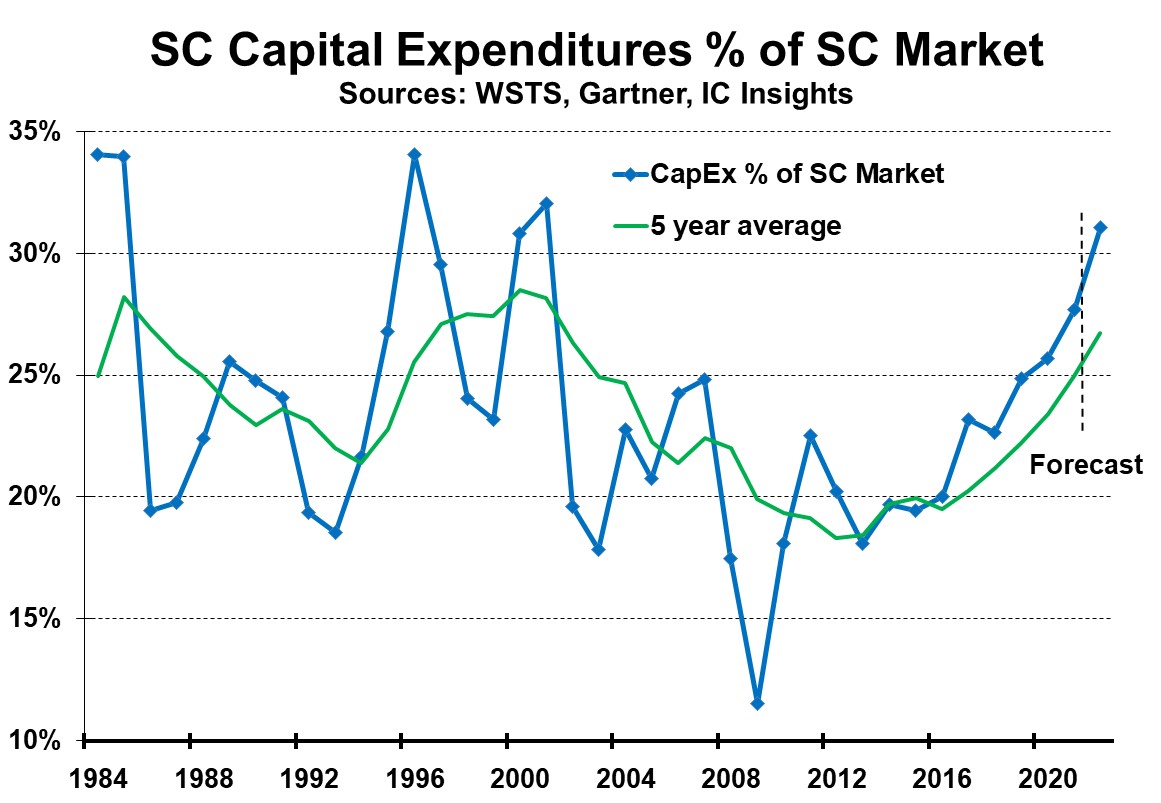

CapEx growth should not be looked at in isolation. Absolute levels of CapEx relative to the semiconductor market give an indication whether CapEx is too high. The graph below shows semiconductor CapEx as a percentage of the semiconductor market on an annual and five-year average basis. Over the last 38 years, from 1984 to 2021, CapEx has averaged 23% of the semiconductor market. The five-year average ratio has ranged from 18% to 28%. The ratio has been on an uptrend for the last several years, with the five-year average reaching 27% in 2022 based on forecasts from IC Insights and WSTS. This data indicates the ratio may be close to a peak, indicating lower CapEx in the near future.

Our conclusion is the increase in CapEx should lead to caution, but not to panic. There is no indication of an end demand bubble, such as with the PC and internet infrastructure. Most of the growth is driven by non-memory companies, which largely produce non-commodity products. But the CapEx growth in 2021 and 2022 should be of concern based on historical trends. Our current forecast for the semiconductor market is 15% growth in 2022 and 5% to 9% in 2023. At the low end, 5% growth in 2023 would be a 21 point drop from 26.2% growth in 2021. This would fit the model, with the 36% CapEx growth in 2021 above the 27% warning line and leading to an over 20-point growth rate decline two years later in 2023.