Shipments of semiconductor wafer fab equipment are expected to grow 2.5% in 2016 after 0.5% growth in 2015 according to the December forecast from Semiconductor Equipment and Materials International (SEMI). Gartner is more pessimistic, with its October forecast calling for fab equipment to decline 0.5% in 2015 and drop 2.5% in 2016. Gartner projects the market will return to growth in 2017 through 2019.

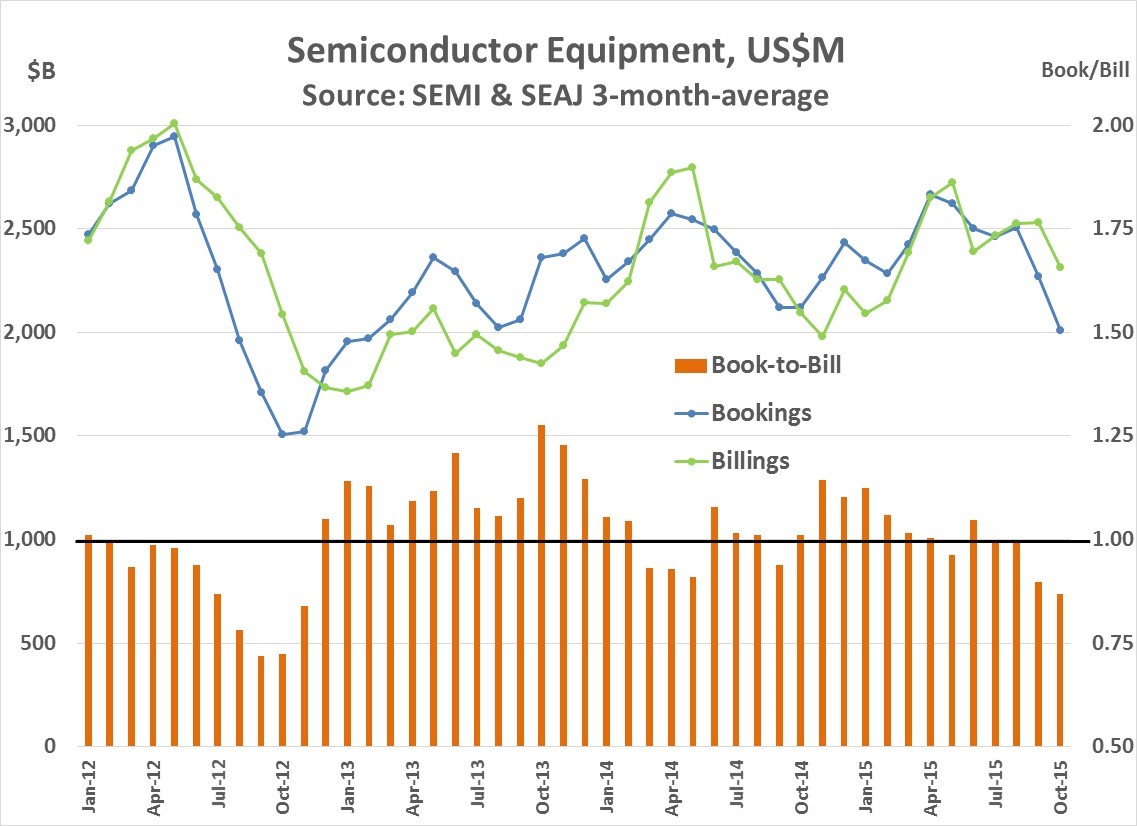

A drop in fab equipment shipments in 2016 appears almost certain based on the combined October data from SEMI and Semiconductor Equipment Association of Japan (SEAJ). Three-month-average semiconductor manufacturing equipment bookings dropped to $2.01 billion in October, the lowest level since February 2013. The book-to-bill ratio was 0.87, the lowest since 0.84 in November 2012. The semiconductor equipment market declined 13% in 2012 and dropped 16% in 2013. We at Semiconductor Intelligence believe the current downturn will not be as severe, with semiconductor equipment down 5% to 10% in 2016 and resuming growth in 2017.

Semiconductor capital expenditures (CapEx) for 2015 are projected to be $63.9 billion, down 1% from $64.6 billion in 2014, according to Gartner’s October forecast. Gartner expects CapEx will drop 3.3% in 2016 before picking up to 5% to 6% growth in 2017 through 2019. Semiconductor capital spending can be grouped into four major segments:

- Foundry companies such as TSMC, GlobalFoundries and UMC.

- Memory companies including Samsung, SK Hynix, Micron and IM Flash (Toshiba/SanDisk joint venture).

- Intel, the largest semiconductor company and dominant microprocessor supplier.

- Other – all other semiconductor companies (numbering in the hundreds).

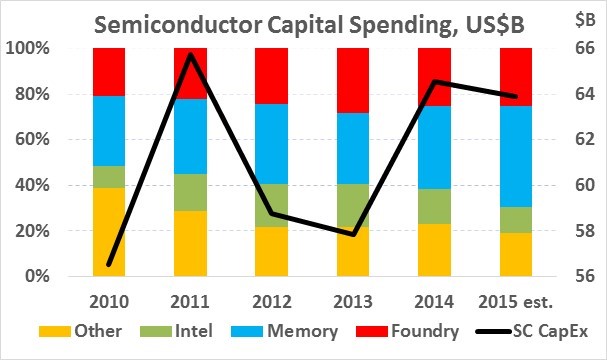

The chart below shows SC CapEx from 2010 to 2015. Total CapEx is based on data from IC Insights (2010 to 2014) and Gartner (2015 estimate). CapEx for each segment is based on company data and estimates for 2015.

CapEx was $54 billion in 2010, more than double the $26 billion in 2009 during the semiconductor downturn. Capital spending increased 25% to $67 billion in 2011. CapEx dropped in 2012 and 2013 before resuming growth in 2014. The four segments show varying trends. The foundry segment has generally been on an upturn, from 21% of the total in 2010 to 25% in 2015. Memory increased from 31% in 2010 to 44% in 2015. The Memory segment should decline in 2016 as both Samsung and SK Hynix plan to cut CapEx. Intel’s portion increased from 10% in 2010 to 19% in 2012 and 2013 before dropping to 11% in 2015. The most significant trend is the Other segment dropping from 39% in 2010 to 19% in 2015. In dollars, Other CapEx dropped from $21 billion in 2010 to an estimated $10 billion in 2015.

What is behind the downward trend in Other CapEx? One major factor is almost all new semiconductor companies adopt a fabless strategy – focusing on design, marketing and sales and leaving manufacturing to outside foundries. Another key factor is many existing semiconductor companies are relying less on their own fabs and more on outside foundries. As shown in the table below, the top three spenders grew CapEx from 2010 to 2014, ranging from 22% for Samsung to 94% for Intel. In contrast, three major semiconductor companies with fabs have significantly reduced CapEx. Texas Instruments, STMicroelectronics and Renesas Electronics all spent over a billion on CapEx in either 2010 or 2011. Each company has been cutting CapEx significantly since, with 2014 versus 2010 down 60% for ST and Renesas and down 68% for TI.

CapEx, US$Billion |

2010 |

2011 |

2012 |

2013 |

2014 |

2014/10 |

Top 3 |

||||||

Samsung |

11.0 |

12.1 |

12.3 |

11.8 |

13.3 |

+22% |

Intel |

5.2 |

10.8 |

11.0 |

10.7 |

10.1 |

+94% |

TSMC |

5.9 |

7.3 |

8.3 |

9.7 |

9.5 |

+61% |

Others |

||||||

Texas Instruments |

1.20 |

0.82 |

0.55 |

0.41 |

0.39 |

-68% |

STMicroelectronics |

1.24 |

1.28 |

1.11 |

0.53 |

0.50 |

-60% |

Renesas Electronics * |

0.90 |

1.05 |

0.56 |

0.37 |

0.36 |

-60% |

* Renesas data for fiscal year ending March of following year |

||||||

Mergers and acquisitions are also leading to decreased CapEx in the Other segment. Combinations of semiconductor companies with fabs leads to a consolidation of manufacturing. The combined company will spend less on CapEx than the individual companies would have spent. In 2010, Renesas Technology and NEC Electronics merged to form Renesas Electronics. Renesas was originally formed by the merger of the semiconductor businesses of Hitachi and Mitsubishi Electric in 2003. Texas Instruments acquired National Semiconductor in 2011.

Recent M&A activity contributing to manufacturing consolidation and lower CapEx includes:

- NXP Semiconductors completed its acquisition of Freescale Semiconductor last week.

- ON Semiconductor agreed to acquire Fairchild Semiconductor last month (see our November post for details).

- Infineon Technologies acquired International Rectifier in January.

Other recent M&A activity does not affect CapEx since the acquired companies are fabless. This includes Avago’s pending acquisition of Broadcom and Intel’s proposed acquisition of Altera.

The trend is inevitable – new fabs will be built by companies with the economy of scale to justify an investment of $5 billion to $10 billion per fab. Thus memory companies, foundry companies and Intel will dominate CapEx. Other companies will continue to upgrade their existing fabs, but few (if any) will build new fabs.