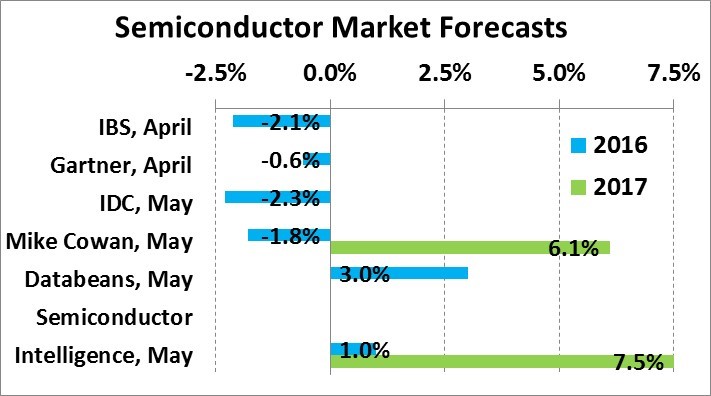

Several recent forecasts for the 2016 semiconductor market point to a decline. The title of this newsletter is the same as we used for our October 2015 newsletter. In October, Semiconductor Intelligence projected the market would grow 1.0% in 2015 despite several predictions of the market going negative. 2015 finished with a slight 0.2% decline. The chart below shows four forecasts in the last two months calling for a negative 2016, ranging from a 0.6% decline from Gartner to a 2.3% decline from IDC. Databeans projects 3.0% growth. We at Semiconductor Intelligence are calling for 1.0% growth in 2016. For 2017 semiconductor market growth, Mike Cowan’s May forecast was 6.1%. We at Semiconductor Intelligence are projecting 7.5% growth.

What is behind the weak 2016 outlook? According to World Semiconductor Trade Statistics (WSTS), the 1st quarter 2016 semiconductor market declined 5.5% from 4Q 2015, the weakest first quarter since the recession in 2009. However, there are signs of improvement in 2Q 2016. The table below shows 1Q 2016 revenue growth versus 4Q 2016 and guidance for 2Q 2016 for the largest semiconductor suppliers.

Key Semiconductor Company Revenue |

|||

Change versus prior quarter in local currency |

|||

|

|

Reported |

Guidance |

|

Company |

1Q16 |

2Q16 |

Comments on 2Q |

Intel |

-8.1% |

-1.5% |

high end +2.2% |

Samsung |

-15.6% |

n/a |

solid DRAM & SSD demand |

Qualcomm |

-18.5% |

0.9% |

high end +8.1% |

SK Hynix |

-17.2% |

n/a |

solid DRAM & SSD demand |

Micron |

-12.4% |

0.5% |

high end +5.7% |

TI |

-5.7% |

5.4% |

high end +10.8% |

Toshiba |

0.3% |

n/a |

|

NXP |

38% |

5.4% |

1Q includes Freescale |

Infineon |

1.0% |

2.0% |

high end +4% |

MediaTek |

-9.4% |

28.0% |

China handset demand |

ST |

-6.5% |

5.5% |

high end +9% |

Renesas |

1.8% |

n/a |

uncertain after earthquake |

1Q 2016 revenues declined from 4Q 2015 for most companies, including double-digit declines for the Memory companies (Samsung, SK Hynix and Micron) and Qualcomm. NXP’s 38% growth is a result of its acquisition of Freescale. The outlook is fairly strong for most companies in 2Q 2016. All but Intel are projecting growth, with Intel’s high end guidance for 2.2% growth. The high end guidance for Qualcomm, TI and ST is in the 8% to 10% range. MediaTek is guiding 28% growth in 2Q 2016 based on strong handset demand from China. Broadcom is not included since it is in the process of integrating its merger with Avago.

The outlook for key end equipment is major factor for the weak semiconductor market in 2016. Gartner’s March 2016 forecast for PC plus tablet units is a 2.5% decline in 2016, following a 10% decline in 2015. Growth is projected at a positive 2.5% in 2017. Mobile phone units are projected to show growth in only the 1% to 2% range. The International Monetary Fund’s (IMF) April 2016 forecast is 3.2% global GDP growth in 2016, only slightly higher than 3.1% in 2015. GDP is expected to pick up to 3.5% growth in 2017.

Forecast Annual Change |

||||

2015 |

2016 |

2017 |

Source |

|

PC + Tablet Units |

-10% |

-2.5% |

2.5% |

Gartner, March |

Mobile Phones |

2.0% |

1.4% |

2.1% |

Gartner, March |

Global GDP |

3.1% |

3.2% |

3.5% |

IMF, April |

Our Semiconductor Intelligence forecast of 1.0% semiconductor market growth in 2016 takes into account the weak end markets. However, the 2Q 2016 outlook for major suppliers is encouraging. The growth acceleration for end equipment and GDP in 2017 leads to our forecast of 7.5% growth in 2017.