The global semiconductor market grew 21.6% for the year 2017, according to World Semiconductor Trade Statistics (WSTS). The market was much stronger than anticipated at the beginning of year. Semiconductor Intelligence tracked publicly available forecasts to determine which was the most accurate. We used forecasts made in late 2016 and early 2017 prior to the availability of the January 2017 WSTS data in March 2017. The winner was Future Horizons with a projected 11% increase in the 2017 semiconductor market. Our Semiconductor Intelligence forecast of 8% was the second closest. Other forecasts ranged from 3.3% from WSTS to 7.2% from Gartner. A booming memory market was the key driver, up about 60% according to WSTS. The semiconductor market excluding memory grew about 9%, closer to expectations at the beginning of 2017.

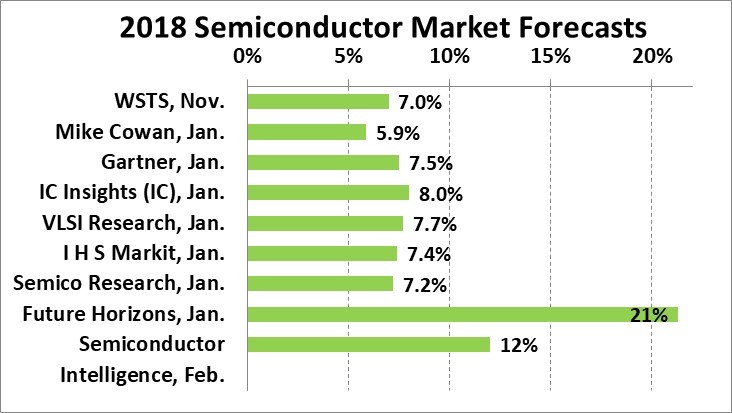

What is the outlook for 2018? The perennial optimists at Future Horizons are calling for 21% semiconductor market growth in 2018, about the same rate as in 2017. We at Semiconductor Intelligence are staying with our December 2017 forecast of 12% growth in 2018. Other recent projections are in a narrow range from Mike Cowan’s 5.9% to IC Insights’ 8.0%.

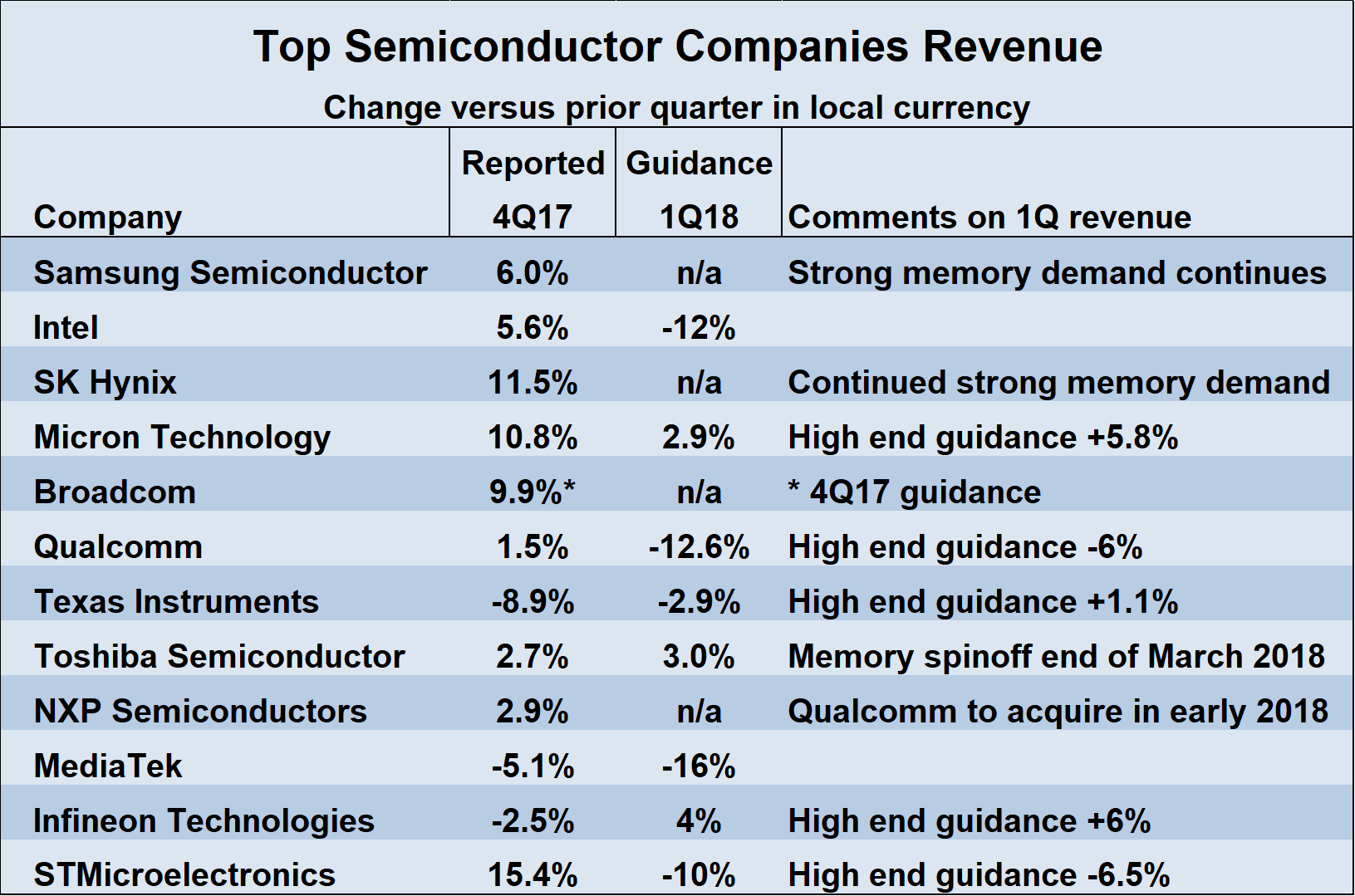

The growth rate of the 2018 semiconductor market is largely dependent on the first quarter. The first quarter is the seasonally weakest, averaging a 3.5% quarter-to-quarter decline over the last five years. Revenue guidance from major semiconductor companies confirms a likely decline in 1Q 2018. Double digit quarter-to-quarter revenue declines are projected by Intel, Qualcomm, MediaTek and STMicroelectronics. The memory companies expect revenue gains, with Micron guiding +2.9% and Toshiba guiding 3.0%. Samsung and SK Hynix did not provide specific guidance, but both expect strong memory demand to continue in 1Q 2018. A weighted average of the revenue guidance from the companies below points to a decline of over 3%. Using the upper end guidance points to a decline of about 2%.

The key 2018 assumptions behind our December 2017 forecast are unchanged:

- Steady or improving demand for key electronic equipment

- Slight improvement in global economic growth

- Moderating, but continuing strong memory demand

- Strong quarterly growth set in 2017 drives healthy 2018

The outlook for 2019 is weaker. As shown in the table below, Gartner expects PC and tablet unit shipments to recover from a 3.6% decline in 2017 to flat in 2018 and 2019. Mobile phone units should bounce back from a 2% decline in 2017 to 2.6% growth in 2018 and slow to 1.1% in 2019. The International Monetary Fund (IMF) January 2018 forecast called for a slight acceleration in GDP growth from 3.7% in 2017 to 3.9% in 2018. 2019 growth remains at 3.9%, healthy but with no acceleration from 2019. Our Semiconductor Intelligence forecasting models show the rate of semiconductor market growth is more closely linked to acceleration or deceleration in GDP than to the level of GDP growth.

| Annual Growth Forecast | 2017 | 2018 | 2019 | Source |

| PC & Tablet units | -3.6% | 0.0% | 0.0% | Gartner, Jan. 2018 |

| Mobile phone units | -2.0% | 2.6% | 1.1% | Gartner, Jan. 2018 |

| Global GDP | 3.7% | 3.9% | 3.9% | IMF, Jan. 2018 |

The strong memory market will probably not continue into 2019. The key question is whether the memory boom will end with a bust (severe declines in demand and prices) or a soft landing (moderation in demand and prices). We currently expect a soft landing in the memory market based relatively steady demand for electronic end equipment. Our preliminary Semiconductor Intelligence for 2019 is low single digit growth of about 1% to 4%.