Japan emerged as the largest supplier of consumer electronics in the 1980s. The Japan surge was driven by lower cost labor than in the U.S. and Europe as well as innovative products from companies such as Sony, Toshiba and Panasonic (formerly Matsushita). By the 1990s much consumer electronics production shifted to South Korea with even lower cost labor and the growth of companies such as Samsung and LG (formerly Lucky Goldstar). Also in the 1990s Taiwan became a major source of production of computers and peripherals.

In the 21st century China has become the dominant source of electronics production. Initially China electronics production was primarily done by subsidiaries or partners of Japanese, South Korean, U.S. and European electronics companies seeking lower cost labor. China-based companies such as Lenovo, Haier, and Huawei have now become major producers. China will continue as the dominant electronics producer for the foreseeable future. Its population of over 1.3 billion will provide a long term source of low cost labor. However several Southeast Asia countries are growing their electronics industries rapidly.

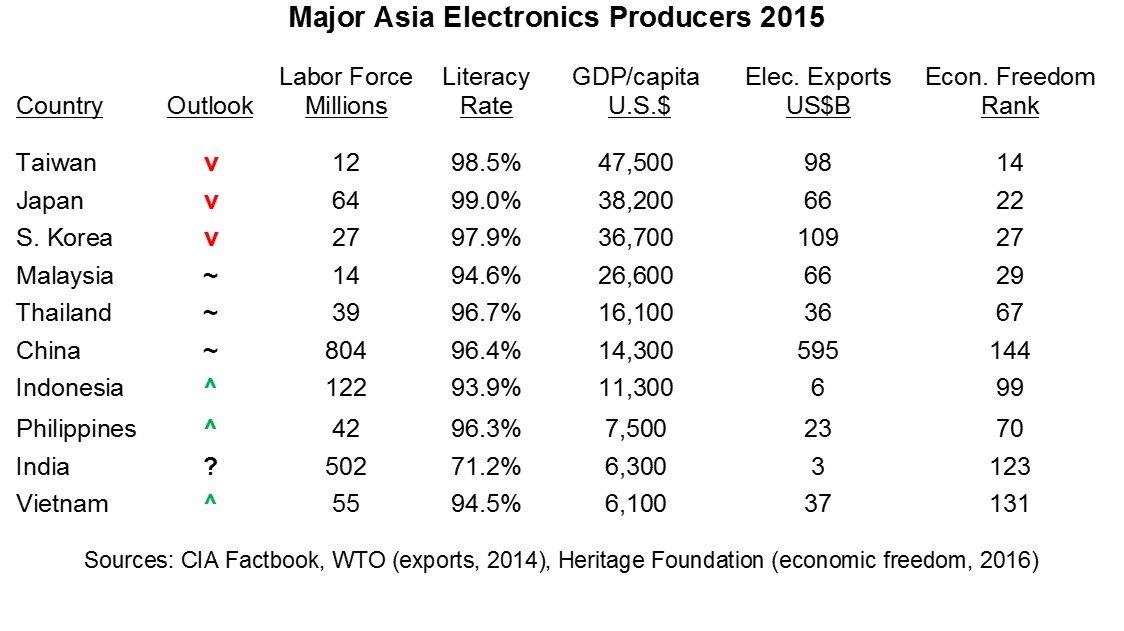

The table below shows major Asian electronics production countries with labor force, literacy rate, GDP per capita, exports of computer and telecom equipment and economic freedom rank. Each country has been assigned an outlook based on our assessment at Semiconductor Intelligence.

The labor force size shows the upper limit on electronics production workers. The literacy rate suggest the education level of the labor force. The countries are ranked by GDP per capita, which is related to the labor cost in each country. Electronics exports reflect the overall electronics production of each country. The economic freedom rank connotes the ease of doing business.

Taiwan, Japan and South Korea have relatively high labor costs which makes growth in electronics manufacturing unlikely, thus they are assigned a down arrow (v) under Outlook. Malaysia’s GDP per capita is higher than most other Asian countries and its 14 million person labor force could limit growth, thus a flat (~) outlook. Thailand and Indonesia have labor costs similar to China. Thailand is limited by labor force size and questionable government stability. China’s growth rate is slowing, earning a flat (~) assessment. Indonesia is poised for growth with a labor force of 122 million people and low electronics exports, justifying its up arrow.

The Philippines, India and Vietnam have the lowest GDP per capita of the listed countries, about half of China’s. The Philippines has long been a major site for semiconductor assembly and test, but it is looking to diversify into more value added electronics production. India has a labor force of over 500 million, but only a 71.2% literacy rate and a low economic freedom rank of 123. Electronics exports are insignificant, with most production for domestic use. India is thus assigned a question mark. Vietnam has shown strong growth (see February 2015 post), has a 55 million person labor force and low GDP per capita – earning a positive assessment (^). Vietnam has a low economic freedom rank of 131, but it is higher than China’s 144. Vietnam is following China’s example as country with a Communist government and a capitalist economy.

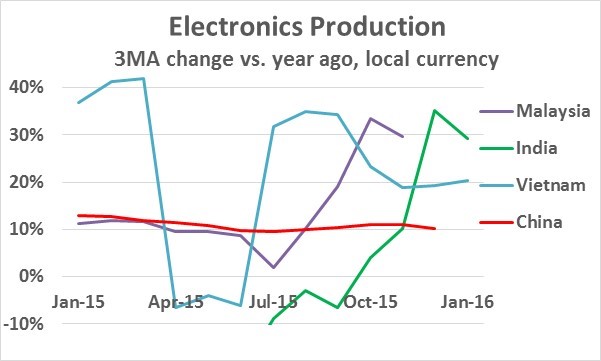

The chart below show electronics production three-month-average change versus a year ago for select countries with available data.

China’s electronics production growth has been slowing from around 13% in early 2015 to about 10% recently. The latest data from Malaysia and India show strong growth of about 30%. India rebounded from declines of greater than 50% in late 2014 and early 2015. Vietnam’s electronics growth is around 20%. Some of the growth factors are short term, but it is a sign of strong growth in other Asian countries offsetting the slowing growth of China.

The shift in electronics production to emerging Asian countries will take several decades to play out. China’s dominance should continue over this period. However countries such as Indonesia, the Philippines and Vietnam are worth watching.