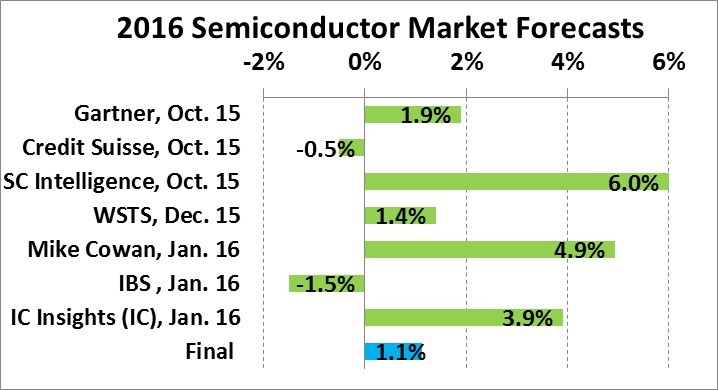

World Semiconductor Trade Statistics (WSTS) is an organization of semiconductor companies created to collect market data. The members of WSTS also meet twice per year to develop forecasts for the semiconductor market. The “forecast by committee” approach of WSTS usually results in conservative forecasts. However, WSTS called it right for 2016. The WSTS forecast released in December 2015 predicted the semiconductor market would grow 1.4% in 2016. The actual growth in 2016 was 1.1%. The chart below shows 2016 forecasts made in the October 2015 to January 2016 period, prior to any 2016 monthly data availability.

After WSTS, the closest was Gartner’s October 2015 prediction of 1.9%. Other forecasts were either higher in the 3.9% to 6.0% range (with our Semiconductor Intelligence forecast the highest) or negative. The 2016 market started out weaker than expected with a 5.3% decline in 1Q 2016 and a weak 0.9% growth in 2Q 2016 – normally a seasonally strong quarter. By mid-2016 basically all the forecasts were negative. Robust 11.6% growth in 3Q 2016 and healthy 5.4% growth in 4Q 2016 turned the year positive.

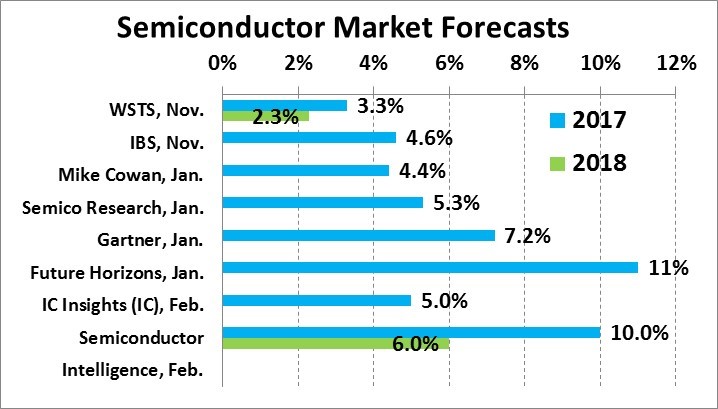

What is the outlook the semiconductor market in 2017 and 2018? WSTS in November 2016 projected 3.3% growth in 2017 and 2.3% in 2018. WSTS appears conservative for 2017, with other forecasts ranging from 4.4% to 11%. Our latest forecast from Semiconductor Intelligence is for 10% growth in 2017 and 6% in 2018.

What is driving the uptick in the market in 2017? One factor is memory prices. Gartner’s Ganesh Ramamoorthy said increasing memory demand and prices added $10 billion to their 2017 forecast. IC Insight’s Bill McClean expects the memory market to grow 10% in 2017, double the rate of the overall IC market.

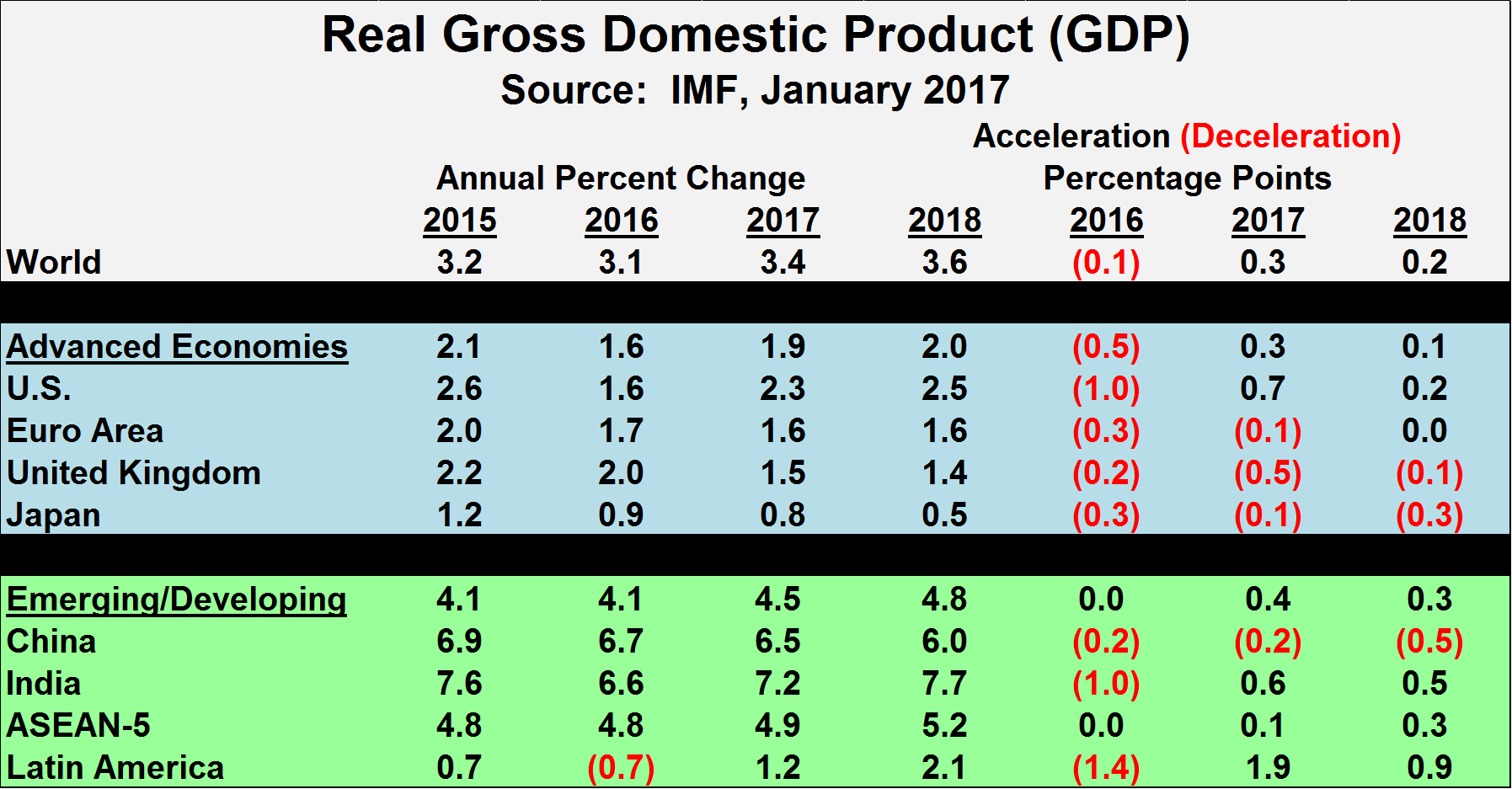

Another driving factor is an uptick in the global economic outlook for 2017 and 2018. The International Monetary Fund (IMF) in January projected global GDP will rise 3.4% in 2017, up 0.3 percentage points from 2016. 2018 is expected to add 0.2 points to bring GDP growth to 3.6%. The advanced economies contribute only moderately to 2017 and 2018 GDP acceleration. U.S. GDP growth should pick up from 1.6% in 2016 to 2.5% in 2018, but still below 2015’s 2.6%. The Euro Area and the United Kingdom are project to show flat to decelerating growth over the next two years after the UK voted to withdraw from the European Union. Japan GDP will remain stuck below 1% annual change.

The drivers for global GDP will be the emerging and developing economies, with GDP expansion accelerating from 4.1% in 2016 to 4.5% in 2017 and 4.8% in 2018. China’s GDP growth rate continues to slow, but should remain above a healthy 6%. India and the ASEAN-5 (Indonesia, Malaysia, Philippines, Thailand and Vietnam) offset China with accelerating GDP growth. Latin America will contribute by rebounding from a 0.7% GDP decline in 2016 to a 2.1% increase by 2018.

The electronics markets driving semiconductor market growth will shift from the old standbys of computing (PCs and tablets) and mobile phones (including smartphones). According to Gartner, PCs and tablets will improve from a 9.9% decline in units shipped in 2016, but only to 1.4% growth in 2018 and 2019. Mobile phones units are also expected to increase no better than 1.4% through 2019.

Unit growth rate |

2016 |

2017 |

2018 |

2019 |

Source |

PCs & Tablets |

-9.9% |

-0.9% |

1.4% |

1.4% |

Gartner, Jan. 2017 |

Mobile Phones |

-1.5% |

0.3% |

1.4% |

0.9% |

Gartner, Jan. 2017 |

IC Insights expects semiconductor sales for the Internet of Thing (IoT) will show a 13.3% compound annual growth rate (CAGR) from 2015 to 2020. Automotive semiconductors are another key driver with a 2015 to 2020 CAGR of 10.3%.

Our Semiconductor Intelligence forecast of a 10% increase in the semiconductor market in 2017 is based on:

-

quarterly market trends driven by a strong second half of 2016

-

moderate improvement in the global economy

-

increasing memory prices

-

modest improvement in the largest applications – PCs, tablets and mobile phones

-

continued proliferation in emerging areas such as IoT and automotive

2018 growth will moderate as memory prices stabilize (or decline) but should be a healthy 6%.